Why the AI Device Wave Is Arriving Slower Than You Think

There has never been a better time to found an AI hardware company. There has also never been a harder time to sell one to a consumer. Both things are true at once, and the gap between them explains a lot about what is about to happen, and not happen, in the next twenty-four months.

The founding side is now broadly understood. A two-person team in Brooklyn or Berlin or Shenzhen can ship a working hardware prototype faster and cheaper than was conceivable five years ago. AI-assisted PCB design tools, including Diode in New York, are compressing schematic and board-layout timelines from months to weeks. Davide Asnaghi, Diode’s CEO, has put the ambition plainly: the company’s goal is "to build an electrical engineer." Their models can already one-shot much of schematic design. Customers include Physical Intelligence and Saronic, and the company has an explicit partnership with Anthropic to help Claude become a better electrical engineer. The combination of off-the-shelf compute, accessible foundation model APIs, falling component costs, and AI-native EDA tools means that what used to be a five-engineer, eighteen-month effort is increasingly a two-engineer, six-month effort.

The result is visible at any AI hardware demo day. Laundry-folding robots. Senior companion devices. Talking plush toys for children. Robotic dogs for security and inspection. Smart cameras with on-device inference. Wearables in dozens of form factors. Humanoid robots that can almost, but not quite, walk across a stage without falling over. Each of these is a real product made by a real team. Each of them has investors. Many of them have impressive demo videos.

How many of them are in daily use a year after launch?

That question is the heart of this piece. Founding is not the same as scaling, and the adoption curve for consumer hardware looks nothing like the adoption curve for consumer software. Most of the AI hardware companies currently raising money are being underwritten on assumptions that do not hold once you look honestly at what consumers will actually buy, keep, and use.

Why now, really

Before we get to the adoption problem, it is worth being precise about why the founding wave is happening at all. Three forces have aligned, and each one matters.

The first is that the software layer of AI is maturing fast enough that the physical interface to it is becoming the next bottleneck. As long as the most interesting thing AI could do was generate text in a chat window, the right form factor was a phone or a laptop. Those already existed. The category did not need new hardware. Once AI starts being useful continuously, ambiently, and across the physical world, the assumption that a screen is the right interface begins to break down. Caitlin Kalinowski, formerly head of AR glasses and VR hardware at Meta and then OpenAI’s hardware lead, has made a version of this argument repeatedly: the AI capability available behind a keyboard is accelerating quickly enough that the digital frontier will close before most people expect, and when it does, the physical world becomes the next battleground. The companies positioning in hardware now have a structural head start.

The second is that a decade of VR and AR investment, which never produced a mass consumer category, did produce something else: a foundational stack of computer vision, SLAM positioning, depth sensing, spatial computing, and human-perception research that is now being redeployed into robotics, autonomous vehicles, and consumer hardware. The technology is largely de-risked. What remains is productization, manufacturing yield, and unit economics. Kalinowski’s view, drawn from leading multiple generations of Quest, Rift, and Orion at Meta, is that consumer VR did not fail because the technology was missing. It failed because the form factor, the cost, and the daily-use case never quite cohered. The technology is now being put to work in problems where the daily-use case is clearer.

The third is that talent is rotating. Computer science enrollment at top US universities has flattened or declined in recent years, while robotics, mechanical engineering, and hardware-adjacent disciplines are growing. This is a lagging indicator, not a leading one, and it will take five to ten years to show up in startup output. But the signal is real. The most ambitious technical builders increasingly think the interesting frontier is physical, not digital. That perception, accurate or not, becomes self-fulfilling. The next generation of hardware founders is forming now.

There is a fourth, less discussed force, and Kalinowski has been the most public voice on it: a coming supply-chain shock on memory. AI data center demand is already consuming HBM and DRAM capacity fast enough to crowd out consumer hardware allocations. DRAM prices rose 80–90% in Q1 2026 alone (Counterpoint Research), with HBM capacity at Micron and SK Hynix fully booked through 2026. Her advice to hardware startups is direct: pre-buy memory now, lock in supply, and prepare to verticalize. First movers who solve this will have a durable cost moat. Late movers will spend the next cycle paying spot prices that wreck their unit economics. This is not a theoretical risk. It is already starting to play out in component pricing.

The adoption problem

The founding barrier is collapsing. The adoption barrier is not.

Consumer hardware has a fundamentally different adoption curve than consumer software. A consumer software product can be tried at zero marginal cost, abandoned without penalty, and re-tried six months later when it is better. The penalty for shipping a mediocre v1 of a consumer app is reputational, not structural. The user moves on and the developer ships v2.

Hardware does not work that way. A consumer who buys a $400 device and finds it disappointing does not buy v2. They tell their friends not to buy v1. The device sits in a drawer. The category, in their mind, is closed for the next three to five years. The Rabbit R1, the original Humane AI Pin, and a long line of consumer hardware launches over the past two decades have proven this dynamic over and over again. Hype cycles in consumer hardware are not free options. They are foreclosures. Every failed launch makes the next launch in the same category harder, not easier, because consumers and retail partners and component suppliers all remember.

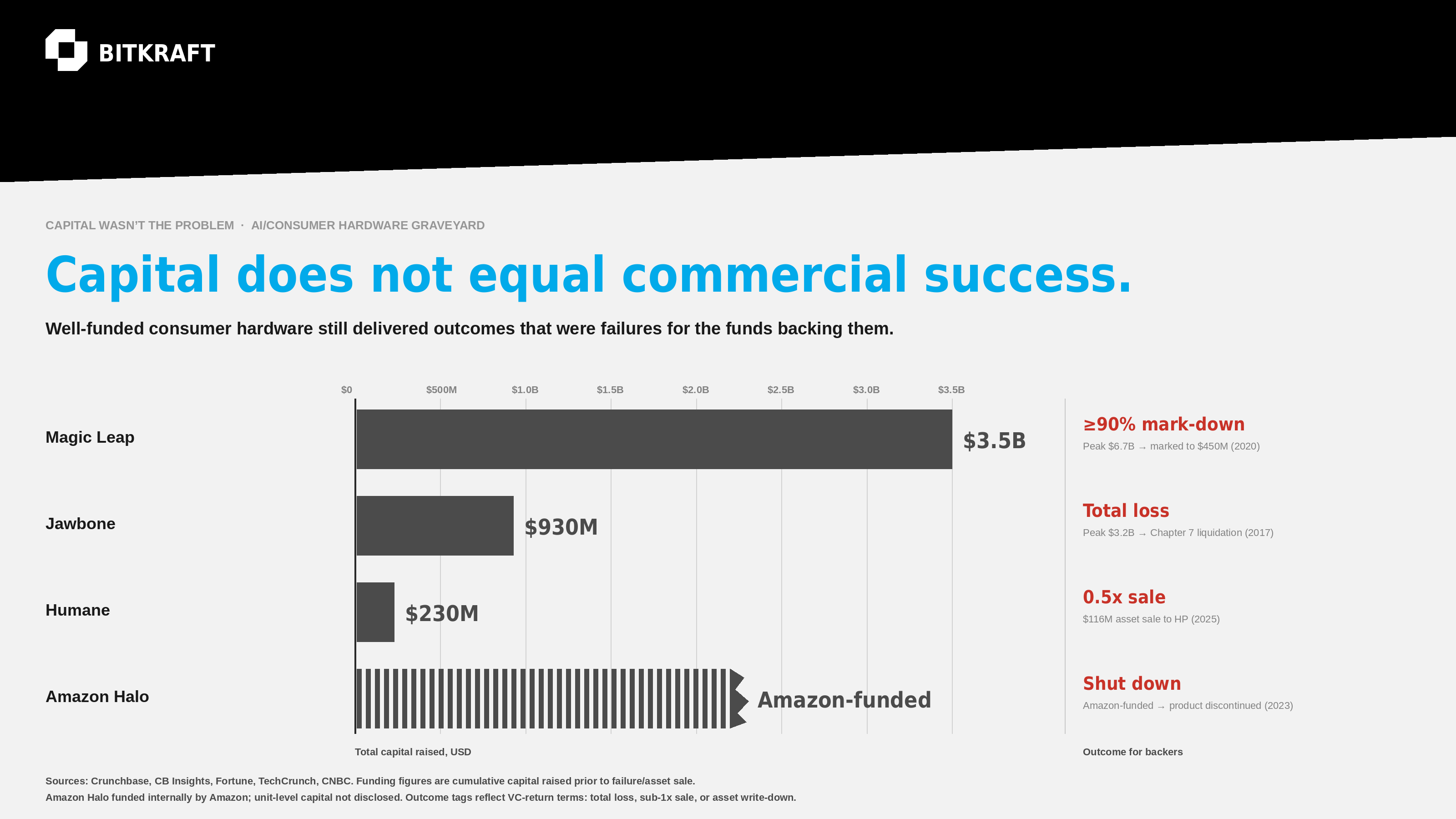

The failures were not for lack of capital. Magic Leap raised $3.5 billion and marked its valuation down by 90%. Jawbone raised nearly $1 billion and ended in Chapter 7. Humane raised over $200 million and sold to HP for less than half of what it had put in. Amazon Halo had the deepest pockets in tech behind it, and got shut down anyway. In each case, the capital was present. The moat was not.

This produces what is best described as the novelty trap. Many of the products currently generating social media virality, the laundry-folding robots, the AI companion devices, the talking plush toys, are extremely effective at producing twenty-second demo videos. They are not necessarily effective at producing daily utility. Viral is not the same as adopted. A category full of Year 1 products without a Year 2 story is a category that will spend the next cycle losing capital, regardless of how compelling the demos look.

The honest test for any consumer AI hardware product is the same three-part question that has applied to consumer hardware for decades. First, does it deliver immediate, obvious utility on day one, in a way the consumer can articulate to a friend? Second, is it reliable enough that the consumer will pick it up on day thirty without thinking? Third, is the price-to-value ratio defensible against the next iteration that will arrive in eighteen months? Most current AI hardware products fail on at least two of those three. Some fail on all three.

A Market Map

To make sense of the current landscape, it helps to put the categories on the same page. The companies in the AI hardware wave can be sorted along two axes: the maturity of the daily-utility case, and the credibility of the route to revenue (consumer-direct versus enterprise or institutional).

What emerges from that sorting is clear. The categories where the daily-utility case is strong and the enterprise route is well-defined, including industrial inspection robotics, warehouse automation, certain medical devices, and defense-adjacent hardware, are genuinely investable today. The categories where the daily-utility case is strong but the consumer route is unproven, including humanoid robots, home robotics beyond floor cleaning, and AI companion devices for adults, are not investable yet at consumer-retail scale. They will get there, but the timeline is five to ten years for most of them, not eighteen months. The categories where the daily-utility case itself is unclear, including most of the wearable AI category and most of the ambient-computing category, are speculative regardless of route to market.

There is one notable exception, and it is worth carving out.

Kids´Toys are different

Children’s products operate on different economics, and the structural reason is that the purchaser and the user are not the same person. A parent buying an AI-enabled toy is buying a combination of novelty, educational signal, and the parent’s own sense of giving their child something modern. The child is the one playing with it. This decouples the daily-utility test in a way that almost no other consumer category enjoys. The toy does not need to be reliably useful every day to justify the purchase. It needs to be charming, safe, and durable enough that the parent does not regret the spend.

The form factor is also established. Plush toys, action figures, and electronic learning devices are not unfamiliar categories the consumer has to be educated into. They sit on shelves in stores that already exist. Mattel and Hasbro and a long tail of smaller manufacturers know how to ship them, and the AI-native entrants are arriving into a distribution system that already works.

The market is meaningful. Globally, the smart/AI toy category is estimated at $14–24B globally in 2025 and growing at 15–20% CAGR. That is small relative to the total consumer hardware market but large relative to almost any other AI hardware sub-category in absolute terms. It is also the category most likely to produce a genuinely large consumer outcome in the next three years. Not the humanoid robot. The talking plush toy.

The Enterprise path

For most of the rest of the landscape, the more credible near-term path runs through enterprise and institutional customers rather than consumer retail. The reason is structural rather than tactical. Enterprise buyers have a higher tolerance for hardware that is reliable rather than delightful. They will accept a thirty-thousand-dollar device that does one thing well, in a way that no consumer would accept a three-hundred-dollar version of the same logic. They have procurement processes that can absorb integration cost. They have IT teams that can manage the device fleet. They have, in many cases, a regulatory or operational driver that makes the device necessary rather than discretionary.

The contrast that gets cited most often is Boston Dynamics. The Spot quadruped robot has more than 3,000 units deployed globally, predominantly in industrial inspection, utilities, and defense contexts. It is not a consumer product, and Boston Dynamics is not trying to make it one. The unit economics work because the customers are paying for productivity gains and safety improvements that are denominated in real money. Compare that to the dozen consumer humanoid robot launches that have happened in the past three years. The technology in many cases is impressive. The consumer use case is not, and the revenue line reflects it.

The pattern holds across categories. AI-enabled medical devices are being deployed in hospitals before they are being sold to consumers. AI hardware for warehouses, logistics, and manufacturing is moving faster than AI hardware for homes. Defense and dual-use applications, controversial as they are in some circles, are some of the largest revenue lines in the entire category. None of this means consumer AI hardware will not eventually arrive. It means the path to revenue for most of these companies, for most of the next cycle, runs through enterprise.

The generational grind

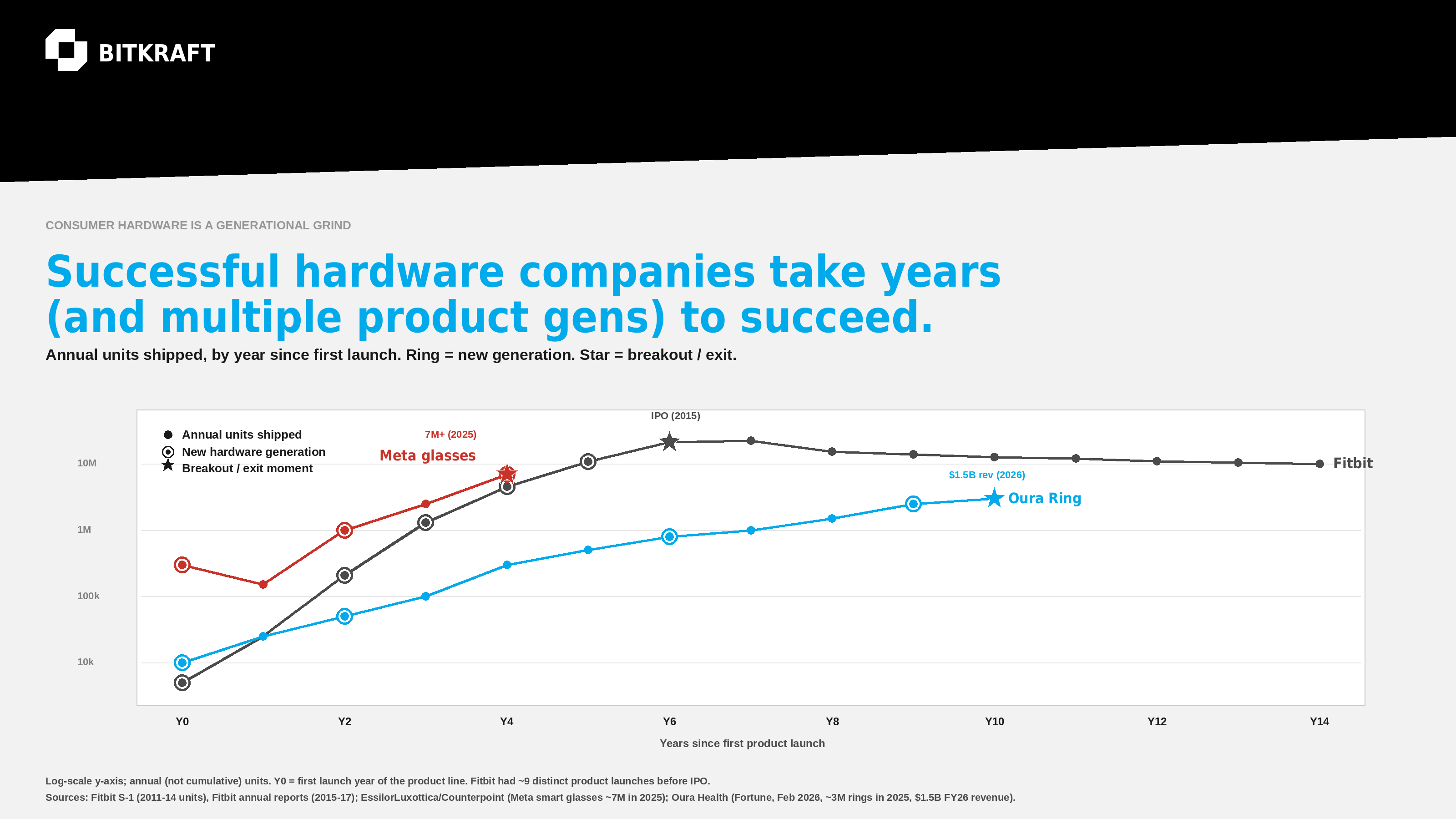

The other pattern that gets under-appreciated is time. The consumer hardware companies that eventually matter tend to look like overnight successes in retrospect and multi-generation grinds in real time. Fitbit shipped roughly nine distinct products across six years before its IPO. Oura took a decade from Gen 1 to reach $1.5 billion in annual revenue. Meta smart glasses flopped as Ray-Ban Stories in 2021, sat in the market for two years, and only broke through at seven million units in 2025 with the third generation. The winners kept iterating on the same product line long after most funds would have written the position down.

This is the counterweight to the novelty trap. The failures die quickly and loudly, in Year 1, and they take their capital with them. The successes take the slow path. Multiple hardware generations, patient capital, and the humility to fix what did not work in v1 before v3 breaks out. That pattern is not what most AI hardware companies raising today are describing to their investors.

A framework for evaluating AI hardware opportunities

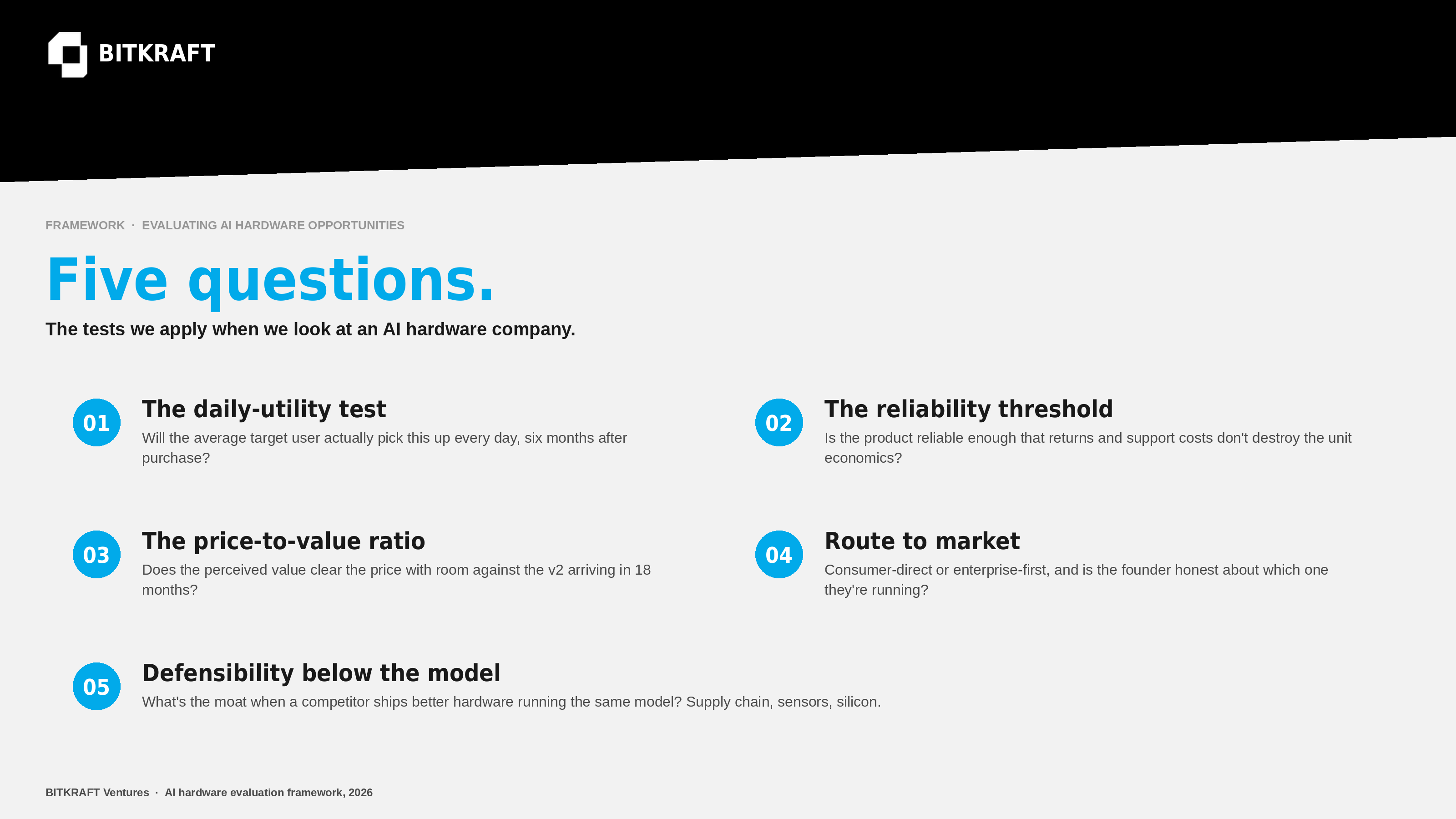

Putting it all together, five questions are useful when looking at any AI hardware company:

The first is the daily-utility test. Will the average target user actually pick this up every day, six months after purchase? If the answer is no, the company is selling novelty, and the long-term revenue line will reflect that.

The second is the reliability threshold. Hardware that breaks, hangs, or behaves unpredictably gets returned. Returned hardware destroys margins and reputations simultaneously. A company that is shipping at a 92% reliability rate is not shipping a product. It is shipping a future support cost.

The third is the price-to-value ratio. Consumer hardware lives or dies on whether the perceived value clears the price by a comfortable margin at launch and continues to clear it eighteen months later when the next iteration arrives. This is harder for AI hardware than for traditional electronics because the software side improves rapidly, which means the price-to-value comparison the consumer makes in month eighteen is against a much stronger v2.

The fourth is route to market. Is this a consumer-direct bet or an enterprise-first bet, and is the founder honest about which one they are running? Companies that try to do both at the same time, with the same product, almost always end up doing neither well.

The fifth is defensibility once the software improves. Hardware moats are not the same as software moats. They depend on manufacturing scale, component lock-in, distribution relationships, and proprietary sensor or actuator advantages. A company whose only moat is the AI model running on the device will lose that moat the moment a competitor ships better hardware running the same model. The interesting questions are about the layers underneath: the supply chain, the manufacturing partnerships, the sensor and silicon choices that produce real cost or performance advantages that compound.

How we think about it

We are watching this category closely. Our investment thesis sits at the intersection of consumer experience and the technology that makes it possible, and AI hardware is a meaningful surface for that intersection over the next decade. We are not yet a committed AI hardware backer in the way that some dedicated deep tech funds are. We are also not dismissive of the category. The honest position is that the framework above is doing real work in how we look at deals. The companies that pass the daily-utility test, the reliability threshold, and the price-to-value test, with a credible route to market and a defensible hardware moat, are rare. They are also genuinely interesting when we find them.

The wave is real. The adoption curve is not what the demo videos suggest. The companies that will matter in five years are mostly the ones that are choosing the harder, slower path through enterprise and institutional customers, and the kids’ toy outliers that have figured out how to deliver charm at the right price. The rest is noise that will resolve itself, expensively, over the next eighteen to twenty-four months. 🔧

Disclaimer

The views expressed herein are those of the author as of the date of publication and are provided for informational purposes only. Nothing contained herein should be construed as investment advice, a recommendation to buy or sell any security, or an offer to provide investment advisory services. Certain statements reflect opinions, expectations, assumptions, and forward-looking views regarding industries, markets, technologies, and business trends, which are subject to change and may not prove accurate. Industry statistics, market data, and company information are derived from publicly available sources, including company disclosures and third-party research providers believed to be reliable, but have not been independently verified and no representation is made as to their accuracy or completeness. References to companies, products, technologies, or market participants are provided solely for illustrative purposes and should not be construed as an endorsement, investment recommendation, or indication of any current or future investment by BITKRAFT Ventures or its affiliated funds. Past outcomes and historical examples referenced herein are not indicative of future results.