India’s digital journey resembles its railways: sprawling, moving, and modernizing at high speed. From packed local trains in Mumbai to slow cross-country routes stitched across language zones to modern new urban metros, the rhythm of India’s internet mirrors this motion – layered and habitual, shaped by who gets on, when they board, and where they go. The mobile phone has become the vehicle: cheap, ubiquitous, and now held by over a billion Indians. This is no longer just urban transit; the next phase of growth is coming from the small stations. While the top of the funnel is widening due to the influx of new users from Tier 2-3 segments, India’s expanding middle class – one of the largest digital consumer segments in the world – is driving growth with its evolving online habits and improving spending propensity.

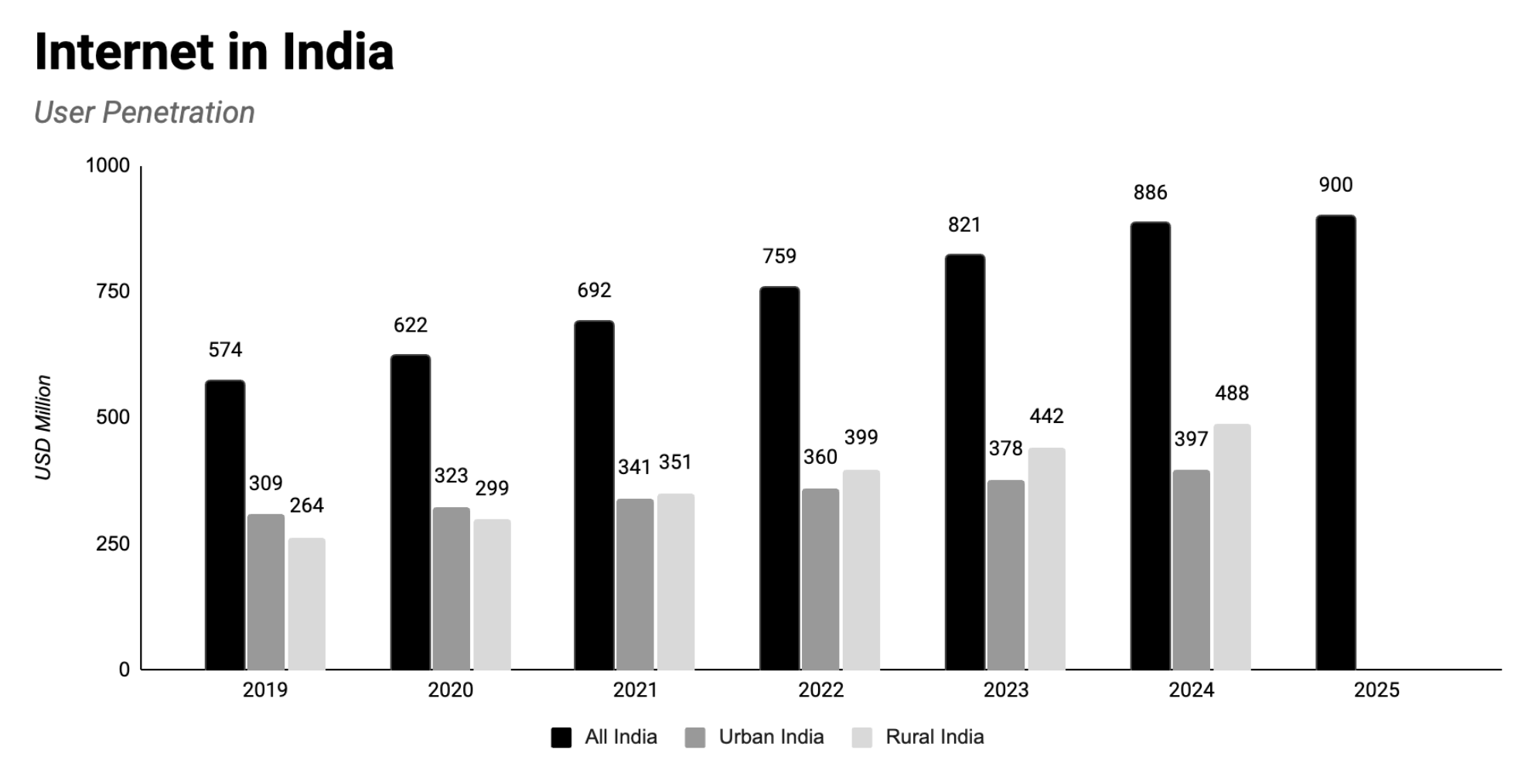

India’s 900 million internet users mostly access the web via mobile. Smartphone adoption continues to grow, putting the country on track for a billion smartphones in use. Over 300 million mobile users remain on feature phones, showcasing both the progress and the endless nature of this journey.

App usage is intense and habitual. In 2024, Indians downloaded 26.4 billion apps and spent 1.1 trillion hours on them – an average of 5+ hours a day. But as with any train platform, a few services draw the largest crowds. WhatsApp, YouTube, Instagram, and PhonePe all serve hundreds of millions of users. Messaging and video are the default behaviours, followed by gaming, payments, and OTT. YouTube remains ubiquitous, while WhatsApp now functions more like public infrastructure than a messaging app.

Generally speaking, new apps face steep drop-offs. Outside the dominant players, the global average 30-day retention is under 2% for social apps and 10% even for sticky verticals like news. Mirroring this, Indians often churn quickly, staying only when the product solves a daily need such as a recurring ritual like entertainment, or a burst-driven behaviour like shopping, events, and emergencies. Uniquely, Indians also tend to revisit apps, creating a cycle of uninstalling and reinstalling based on renewed interest.

Monetisation remains inconsistent. The average revenue per user (ARPU) is structurally low across categories: $24/year for telecom, $2/year in mobile gaming, $22.7/year in streaming video subscriptions, and $170/year for e-commerce. Direct consumer spend is highly price-sensitive, with most users opting for free, ad-supported models. Still, users do pay when value is clear and the tide for monetisation is changing for cases such as live sports, companionship and dating, or educational subscriptions. More often, monetisation flows indirectly via ads, cross-sell, or acquisition funnels.

In 2016, the introduction of United Payments Interface or UPI – a digital payments infrastructure project led by the government-owned Reserve Bank of India and the Indian Banks Association – unlocked India’s payment capabilities at scale. UPI is a real-time payment system that allows users to instantly transfer money between bank accounts using a virtual address (which looks like an email ID), a registered phone number, or a simple point-of-sale QR code. It eliminates the need to share sensitive banking information. On the back of this tech, a slew of Indian fintech companies developed third party payment apps like PayTM and PhonePe. These have gone on to become some of the most crucial and frequently used services in the country.

As of 2024, the UPI platform has over 500 million active users. In May 2025 alone, UPI processed $293 billion across nearly 19 billion transactions, with an average ticket size of just $18. Its rise has made micro-spending seamless and in-app conversions smoother, even for first-time smartphone users. India’s digital economy is powered by products that create daily habits, solve for trust, and adapt to regional patterns. The winners there are like local trains – not sleek or premium, but packed, reliable, and always in demand.

If India’s internet once felt like a library or cinema hall, it has grown to resemble a mela; a sprawling bazaar that is multilingual, full of noise, diversity of belief, and commerce. From astrology consults and devotional livestreams to cricket quizzes, anime fandoms, and voice-first dating apps, India’s digital platforms have shifted from a model of passive consumption to participatory experiences.

The 2016 launch of Indian telecommunications company Reliance Jio was one of the catalysts. As access deepened across Tier 2 and 3 towns, a mobile-first, expressive audience came online. What began with Astrology, Bollywood, Cricket, and Devotion, has exploded into a many-headed hydra. Each speaks its own language, taps its own behaviour loop, and opens a different door into India’s attention economy.

This evolution has made interactive media a core engine of digital growth. The sector now spans spiritual tech, audio storytelling, vernacular video, live streaming, fan platforms, and dating. Despite format differences, these businesses share key traits: high-frequency use cases, emotionally sticky engagement, and culturally native monetisation.

While gaming increasingly targets a global player audience, interactive media remains anchored in India. Rather than chasing mass viewership, these platforms go deep monetising belief, fandom, and routine.

As the ecosystem evolves, we can see Indian companies across categories start to occupy niches with a local-first approach and get on track to become billion dollar businesses. This is shifting the Indian ecosystem ever more towards local champions and away from the grip of international entities. Case in point, platforms like KukuFM, FRND, and AppsForBharat have established leading market positions by embedding localisation not just in language but in tone, UX, and pricing.

While gaming increasingly targets a global player audience, interactive media remains anchored in India. Rather than chasing mass viewership, these platforms go deep monetising belief, fandom, and routine through tipping, bookings, subscriptions, and e-commerce. UPI and in-app storefronts have made this viable even at low price points. Moreover, UPI offers an Autopay feature, which enables direct-debit of subscriptions, and has demonstrated to be a gamechanger in improving the spending propensity of Indian users. Seeing what happens in video entertainment could be a strong pointer to what we could see happening with video games next: local game studios building specifically for this highly diverse yet distinct Indian culture.

In the digital mela of India, faith has found a front-row seat. If astrology is where users seek individual guidance, devotional platforms offer collective belonging. Together, they form the foundation of India’s spiritual internet, which is highly personalised and built on trust. What was once a slow, offline system is now fast, transactional, and mobile-native.

Platforms like AstroTalk, AppsForBharat, Vama, and Utsav have brought rituals, consults, and temple experiences online, converting belief into a durable, monetisable use case. For example, AstroTalk alone now handles 4.5 million paid sessions monthly, with FY24 revenue at $82 million. Consults are priced per minute, with average session values between $3 to $8. Users return multiple times a month, especially around life milestones, driving strong lifetime value (LTV) from a narrow pool of power-users. High ARPU clusters remain among older and diaspora users, who maintain religious routines across geographies. Diaspora markets like those in the US, Canada, and UAE are high-contribution zones across both verticals.

Ritual bookings, donations, and e-commerce drive revenue, spiking predictably during events like Navratri or the annual Kumbh Mela. Bundled services deepen engagement. AstroTalk layers e-commerce and e-prayers into consults. Vama and Utsav offer virtual temple visits, streak-based gamification, and spiritual merchandise. Voice and vernacular drive scale: platforms offer live consults and rituals in multiple Indian languages, often in audio-first formats. AI is beginning to shape content recommendations and match users to astrologers or rituals, though this is early-stage. While devotional tone and trust remain non-negotiable, some platforms are cautiously experimenting with AR overlays, voice-guided home altars, and algorithmic personalisation.

In this segment we observe that monetisation is less about volume and more about intensity. Transactional behaviour is event-driven, price-insensitive at the point of emotional need, and often repeated. However, supply-side quality remains a constraint: astrologer professionalism, ritual authenticity, and cultural sensitivity directly impact retention. Platforms invest in training, vetting, and tone to preserve user trust. While large early raises in the market signal belief in the category’s fundamentals, long-term defensibility will depend on deep localisation, platform credibility, and diaspora monetisation. In a crowded digital mela, we believe that faith remains a high-intent use case – predictable, personal, and culturally sticky.

Historically, India’s cultural life has been a constant performance; it is colourful, crowded, and alive with music, drama, and storytelling. From prayers to podcasts, the same instincts for ritual and narrative have found a home in the country’s audio and video ecosystems.

But the crowd has changed, and so has the performance. The old broadcast model has fractured into a constellation of tents: audio fiction, vernacular video, livestreamed fandoms, new short form drama and niche genres like anime. Each caters to its own audience, speaks its own language, and monetises differently.

The next 100 million users will not behave like the first. They are language-specific, payment-sensitive, and culturally distinct.

For content platforms, the real prize is depth of content, engagement, and monetisation. Platforms that go deeper, rather than broader, are winning. Kuku FM, Pocket FM, and Pratilipi have found loyal audiences through serialised audio and video in regional languages. Low-cost subscriptions and vernacular UI have made scale viable in India. While diaspora listeners in the US may drive higher initial ARPUs than domestic cohorts, Indians have shown immense appetite with domestic players like Kuku FM, with nearly 10 million paying users, seeing superb returns from Tier 2 and Tier 3 India. Pratilipi, with approximately 20 million MAU blends longform fiction, comics, and audio stories into a sticky flywheel. Their IP extensions – from audiobooks to print to theatrical – signal how local storytelling is building cross-format value.

In short-form video, Kuku & Pocket lead the race in regional microdramas, audio, and narrative content. There is also early stage activity with newer entities like ChaiShots and FlickTV also serving this market. This segment serves over 300 million MAUs, with more than 95% of content being consumed in local languages across platforms. The startup ecosystem here is booming with hyperregional content services like Stage, showing that localised long-form content can deliver high LTV even with modest scale. We also see larger conglomerates seeking to establish beachheads in this segment, evidenced by acquisition of MX pLAYER by Amazon. On the whole, operators in this segment avoid mass content, opting instead for frequent releases optimised for low bandwidth and telco bundling to retain their niche.

Anime is the outlier that proves the niche works if the fanbase is deep. Crunchyroll’s growth in India is powered by Hindi dubs and localised campaigns. In fact, India will soon account for 60% of global anime demand growth. Paid users remain modest, but engagement rivals gaming at over 60 minutes per session, driven by binge-watching. Cosplay events, merchandise, and theatrical releases are turning anime from a fringe interest into a premium vertical.

Elsewhere, livestreaming rituals, concerts, and talk shows draw long watch times but limited monetisation unless layered with donations, tipping, or premium access. This format holds attention longer than reels, but the revenue still concentrates around superfans.

Together, these ecosystems form the storytelling stack of India’s interactive internet: audio for solitude, video for leisure, livestreams for belonging. Monetisation is uneven, but loyalty is high. As new users enter the mela, content remains their first stop and, increasingly, their favourite stall.

We believe content depth and distribution scale will define the next wave of interactive media in India. Platforms that cluster around genres, regions, or formats like serialised audio or dubbed anime will see higher retention, lower CAC, and stronger monetisation, especially with microdramas leading the way. The next 100 million users will not behave like the first. They are language-specific, payment-sensitive, and culturally distinct. Models that combine vernacular UX with episodic monetisation (e.g. Pocket FM), cross-format IP and high sub revenue (e.g. Kuku), or diaspora-friendly dubbing (e.g. Crunchyroll) are better placed to survive saturation. Over time, the content stack will fragment further, less like a single tentpole OTT model and more like a cluster of interlinked verticals, each with its own rhythm, rituals, and revenue base with interactivity being the key differentiator as monetization explodes.

If content is the music of India’s digital carnival, fandom is the dancing: loud, chaotic, improvised, but deeply personal. Nowhere is this more visible than with cricket, Bollywood, and anime, where parasocial attachment, meme culture, and digital rituals fuse into high-frequency engagement.

Bollywood fandom remains the most visible, fuelled by short-form video platforms and WhatsApp virality. Trailer drops and controversies generate traffic spikes, with meme formats and remix culture extending a film’s shelf life well beyond release. Fan pages like Instant Bollywood now reach 50M+ followers. Yet, monetisation is thin and most of this energy lives on generalist platforms. AI-generated celebrity avatars, paid shoutouts, and gated fan groups are being tested, but few models have scaled beyond brand integrations.

Cricket, on the other hand, has built year-round engagement. Platforms like JioCinema transformed the Indian Premier League (IPL) – the country’s largest cricket sporting event – into a digital-first viewing experience, layering alternate feeds, multi-language commentary, and real-time stats. Fantasy platforms like Dream11 cater to over 200 million users, converting their attention into spend through microtransactions and leaderboards. CricHeroes brings grassroots matches online for over 30 million users. Startups like Quidich and Quintar are layering spatial computing and AR to make cricket even more interactive. Monetisation here is real. The IPL was a key factor in Dream11’s revenue of $750M+ in FY23, supported by diaspora viewership, fan-created content, and new data-led overlays.

Anime fandom is a quieter revolution, but no less intense. Viewership has exploded through Hindi dubbing and community-led promotion. Average session times exceed an hour, and platforms like Crunchyroll are embedding local campaigns, events, and dubbed commentary to deepen attachment. Offline engagement is catching up: Delhi and Chennai Comic-Cons now register thousands of cosplayers, and anime theatrical releases like Nezha 2 have begun to see stronger box office returns. Merchandising and local community events hint at a K-pop-style monetisation path, though India lacks a domestic production ecosystem.

We believe India’s fan ecosystems are evolving from broadcast-era passivity into digitally active, monetisable communities. Time spent is no longer a proxy for value; platforms must convert fandom into spend through gamification, social layers, and commerce. Cricket leads this shift, blending streaming, fantasy, and second-screen formats to create high-velocity monetisation. Bollywood remains event-led but under-monetised, with opportunities emerging around AI-led interactions and niche fandoms. Anime is India’s most export-aligned subculture: small in monthly active users (MAU) but high in intensity, LTV, and merchandise upside. As these ecosystems deepen, we expect fan platforms to act less like media companies and more like loyalty engines, which are personalised and increasingly community-owned.

In India’s internet ecosystem, dating and social discovery have set up a tent of their own – half game, half socialising ritual. What began with Tinder in metro cities has grown into a multiform ecosystem, from women-first apps and voice-led flirting games to regional language matchmaking with the polish of product-led design.

India’s dating sector now generates over $500 million in annual revenue, projected to cross $870 million by 2026. Tinder and Bumble remain influential, especially among urban youth. But the most interesting shifts are coming from Indian platforms. Aisle, for instance, built a reputation around long-term intent, not swipes, and now offers vernacular apps like Arike and Anbe. These serve Malayali and Tamil users in their own cultural idioms, mixing modern UX with the tonalities of matrimony.

Elsewhere, FRND has reimagined what dating can look like in Tier 2 and 3 India. Voice chats, pseudonymous game rooms, and regional language banter drive high-frequency use. By branding itself as a pre-dating platform, not a dating app, FRND avoids social stigma and taps into the cultural realities of courtship. Monetisation happens through virtual gifting and feature unlocks, not subscriptions.

Trust remains a gating factor. Products have evolved to meet this: TrulyMadly uses “Trust Scores,” Woo supports voice calls without number exchange, and GoGaga leans on referral networks. Women-first design is no longer optional. Verified profiles, content moderation, and privacy tools are now central to product-market fit, especially with skewed gender ratios (3:1 in many apps).

As behaviour evolves, so do formats. Static profiles are giving way to voice notes, video intros, and interactive features like games and group events. Some apps now position themselves closer to social discovery than dating. HiHi, for instance, encourages serendipitous friendships rather than explicit romantic intent.

Pricing models have diversified. Global players lean on subscription tiers and consumables; Indian platforms prefer hybrid and freemium models. Aisle monetises via “invites” and FRND via daily activity loops. Across the board, paying users are a small but valuable cohort, driven by emotional need and high intent.

The category remains fragmented by language, region, and relationship goals, but the throughline is clear: apps that reflect India’s lived social dynamics are scaling. Whether through flirt games or voice-led courtship, the next wave of interactive platforms curate and choreograph the way users form relationships.

We see India’s dating and social discovery market evolving toward format-specific depth rather than broad match volumes. Voice-led, regional, and pre-dating experiences continue to outperform swipe-based models in Tier 2 and 3 cities. Monetisation skews toward power users, with gifting, access features, and trust-based tools offering stronger ARPU than subscriptions alone. Platforms that reduce social friction through vernacular design, pseudonymity, and built-in safety will unlock both new cohorts of women and monetisable intent from male users.

Alongside dating, a parallel use case is emerging: AI companionship. In small-town and semi-urban India, loneliness is rising, driven by migration and isolation from traditional community networks. For many young men aged 18–35, especially in Tier 2 cities, voice-based AI chatbots offer a quiet outlet: someone to talk to about business, stress, and beliefs, or just to share a cup of tea with. More than romance, these services are conversational outlets. Voice is key; users want to speak, not type.

We expect this category to deepen as India enters a vernacular AI supercycle. Advances in speech synthesis, local language natural language processing (NLP), and multimodal agents will expand use cases across companionship, emotional wellness, coaching, and everyday social chatter. Early apps in this space already report 200,000–300,000 MAUs with encouraging payer conversion. Over time, we believe the monetisation opportunity will widen, especially as AI companions move from novelty to daily ritual in markets where intimacy is scarce but attention is available.

As this frontier expands, we expect the category to bifurcate: one path toward social networks with pre-dating and dating features, and another toward trust-based digital matrimony. For either to scale, product defensibility will depend not just on moderation and gender balance, but also on voice tech, emotional intelligence, and cultural fluency. The real opportunity lies in serving India’s unseen majority – not with content, but with conversation.

The word jugaad doesn’t have a perfect English equivalent. It loosely means a clever fix, a hack, or a workaround. But in India, it’s best understood as a mindset: an instinctive drive to solve problems with limited resources, blending ingenuity with pragmatism. Over time, jugaad has evolved from a survival tactic into a business principle that values iteration over perfection and scale over polish. It’s how India built world-class IT services without world-class infrastructure, how local brands cracked rural distribution without modern retail, and how digital payments leapfrogged plastic cards into mobile-first UPI.

In many ways, India’s gaming industry was shaped by the same DNA. Its earliest wave was born in PC cafés and scrappy dev rooms, held together by constraint, ambition, and a willingness to learn by doing.

Game development in India is generally thought to have begun in the late 1990s, with studios like Nazara, IndiaGames and Dhruva Interactive. IndiaGames produced early mobile titles in the pre-smartphone era, along with console releases like Hanuman: Boy Warrior for PS2 and Bioshock: Mobile, a now-obscure adaptation of one of gaming’s most iconic IPs. At the same time, Dhruva in Bangalore quietly became one of the global leaders in art and development services, pioneering the country’s reputation for quality outsourcing in games.

Most notably, Nazara Technologies started out by serving mobile value‑added services for telecom firms. Nazara licensed celebrities like Sachin Tendulkar and Hrithik Roshan, and IPs like Chhota Bheem, partnering with EA to distribute mobile games across South Asia. These early licensing deals and their mobile content strategy positioned them not just as a games exporter, but as proof that a profitable Indian gaming company could exist and scale. In 2021, Nazara went on to become India's first publicly-listed gaming company.

By the early 2000s, other players emerged: Lakshya Digital and Games2Win laid down foundations across both services and original IP. These formative years were scrappy and uneven, but they seeded talent across multiple verticals and built India’s earliest cross-functional teams in game production.

The next inflection came between 2008 and 2011, when global giants began to take India seriously – not just as a potential market, but as a base of operations. Zynga, EA, and Ubisoft all set up major centres in India, variously in Bangalore, Hyderabad, and Pune. Their arrival reshaped the industry. Zynga, in particular, brought live operations and monetisation practices at global scale. It was here that many Indian game professionals first encountered the rigor of metrics-led design, content pipelines, and retention systems. These studios became finishing schools for an entire generation of Indian developers, who would later go on to found the country’s most successful gaming startups.

That lineage is direct. Moonfrog and PlaySimple – two of India’s largest mobile gaming exits – were both founded by former Zynga leaders. Their success demonstrated that Indian teams could not only run games, but build them, scale them, and monetise them independently.

And yet, for most of the 2010s, India’s gaming industry remained underestimated. It was still seen as a back office: a place for low-cost art and QA. Few believed that original games could be built, scaled, or monetised locally. Users were plentiful, but spending was negligible. For most global companies, India was a download market, not a revenue one.

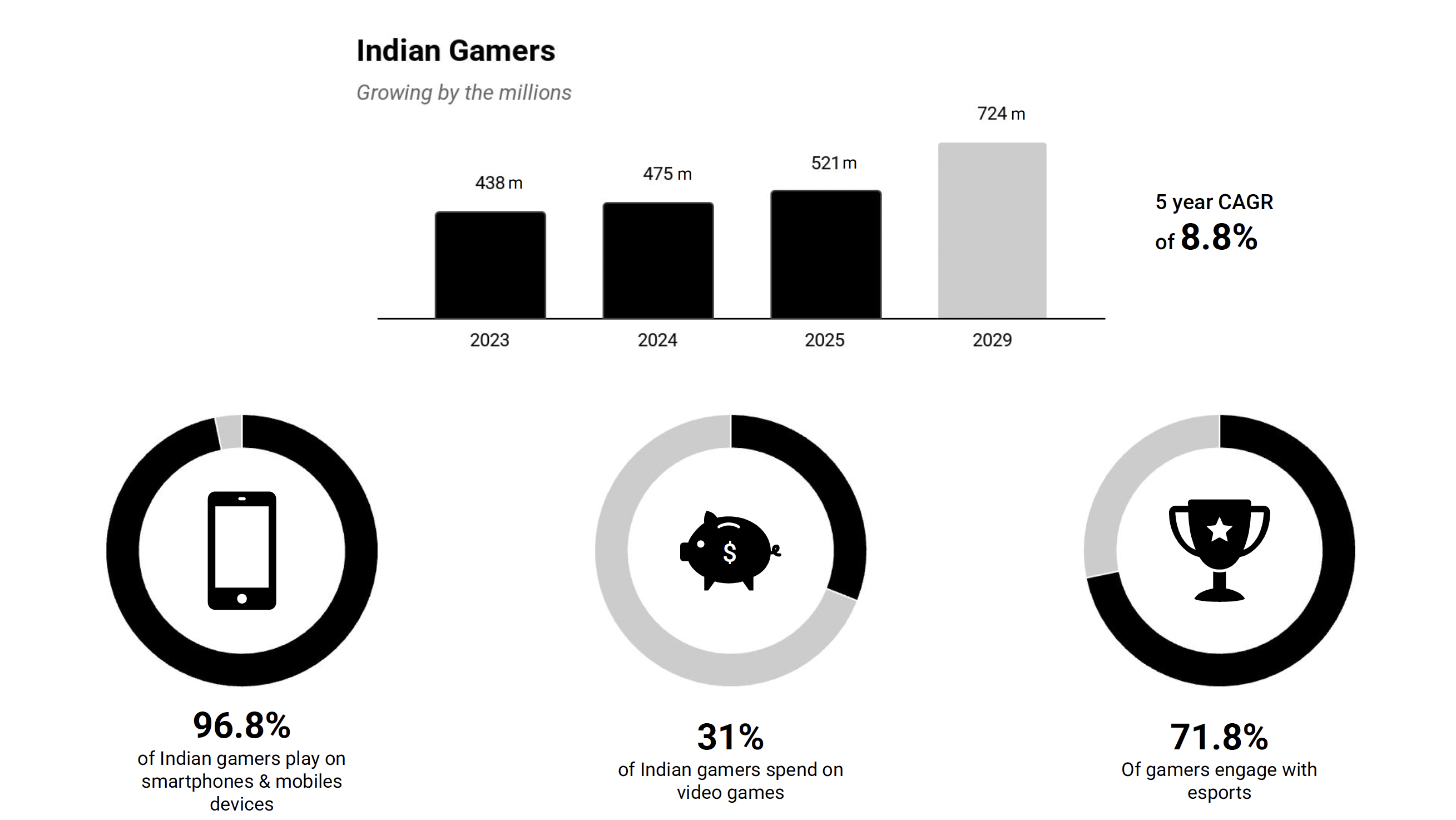

That picture has now changed. The pandemic marked a turning point, catalysing the next wave of gaming in India. A new generation of studios emerged, seeking to not just serve global clients, but to build games for India, from India, or with India. The games market has more than doubled in 3 years, reaching $3.8 billion in FY2024, with $900 million coming from video games and the lion’s share of what’s left from real money gaming (RMG) and fantasy betting. But these top-line numbers only tell part of the story. What began in LAN cafés and live ops studios has evolved into a layered, adaptive ecosystem that is still shaped by the same instincts that defined its origins: speed over polish, iteration over playbooks, and scrappiness as strategy.

India’s gaming boom is inseparable from its smartphone revolution. As affordable Android devices flooded the market across the 2000s and data costs declined, driven by intense telco competition and the Jio effect (the transformative impact of Reliance Jio's entry into the telecom market, particularly its launch of affordable 4G services in 2016), millions of Indians came online for the first time. But unlike the West, where digital adoption began with desktops and broadband, India leapfrogged straight to mobile. The smartphone became the default device for browsing, banking, socialising, and gaming.

Around 96% of Indian gamers play on mobile. The country is the world’s largest market globally by game downloads, with mobile accounting for roughly 80% of total gaming revenue, a figure shaped by the low hardware penetration of PCs and consoles.

What works on mobile in India tends to share some common traits: short sessions, lightweight installs, offline support, and compatibility with low-end devices. These factors have given rise to an ecosystem dominated by casual games, social play, real-money apps, and increasingly, mid-core titles tailored for sub-premium Android hardware.

Console adoption remains minimal. Only a few hundred thousand PS5 units have been sold nationwide, constrained by high hardware and software costs. PC gaming, while eternally growing among urban enthusiasts, is still a niche at around 31 million PC gamers. Combined, these platforms account for only $100 million in annual revenue.

For most of the 2010s, India’s gaming industry remained underestimated. Users were plentiful, but spending was negligible. For most global companies, India was a download market, not a revenue one. That picture has now changed.

Once upon a time, the stereotypical Indian gamer used to be a teenage boy in a metro city, playing Counter-Strike at a LAN Cafe or on a shared Android phone between classes. That image is now outdated. Today, the average Indian gamer is more likely to come from a Tier 2 or Tier 3 town than a metro, and while men still form the majority, women now account for 44% of India’s mobile gaming audience, consistently increasing from previous years.

This behavioural shift has roots in India’s broader digital evolution. 70% of gamers are 16 to 24 years old. Many of them have never owned a desktop, never played console games, and/or never learned to browse the web with a mouse. They came online through mobile-first platforms like Instagram Reels, YouTube Shorts, WhatsApp forwards, UPI payments, and gaming simply slotted into the same user flow. For these users, games are not a separate category of media, but an extension of always-on mobile behaviour. Gaming competes not with traditional entertainment, but with scrolling, messaging, and streaming.

As a result, India’s most popular games reflect familiarity, simplicity, and cultural embeddedness. Casual board, puzzle, and arcade titles dominate the charts, with Ludo King remaining one of the most-played games in the country. These games are lightweight, free-to-play, and built for low-end devices and patchy data, making them ideal for first-time users.

Beneath the casual layer, a new segment has taken hold: the midcore mobile gamer. Games like Battlegrounds Mobile India (BGMI) and Free Fire have built large, loyal followings, especially among users aged 18 to 25, drawn by competitive multiplayer play and progression systems. These players are spending more time in-game and more money, with 2.2x higher ARPPU than casual gamers.

Streaming and esports have amplified this shift. In India, the gaming funnel often starts with curated discovery, typically from watching a Let’s Play video or following a favourite creator. Platforms like YouTube and Instagram serve as on-ramps to gaming, especially for titles that offer competitive depth or cultural cache. For many users, the aspiration to stream, compete, or be part of a fandom is now a core motivator to engage and spend. While esports tournament organizers are still evolving, companies like Nodwin have taken a large lead for being the synonyms with an Indian esports brand. We do not foresee a lot of early stage interest in the same way as we have seen globally, but India is still ripe for building new IP formats around games.

Crucially, India’s gaming audience is still expanding. As smartphones penetrate deeper into rural India, and as more women adopt gaming as a regular digital activity, the market is diversifying in age, geography, and play style. This makes the Indian userbase one of the most dynamic and unpredictable in the world. It means founders and investors alike are building for a market in motion – where audience composition, platform behaviour, and monetisation potential are all changing in real time.

For years, RMG and fantasy sports platforms underwrote a large part of India’s gaming economy. At their peak, they accounted for 60% to 70% of total market value, led by platforms like Gameskraft, Dream11, Games24x7, Ace2three, WinZO, MPL and Zupee. Fantasy sports and skill-based cash games offered familiar, competitive experiences and capitalised on India’s low customer acquisition cost, high smartphone penetration, and deep-rooted affinity for casual real-world gambling. Revenue came from rake fees and entry commissions, supported by a high-frequency, high-churn user base. The RMG universe in short is divided into three categories: fantasy sports, card games (Rummy, Poker), and multi-games platforms (with multiple games like Ludo).

For a time, it appeared that RMG would serve as the monetisation wedge for Indian gaming. VC interest was high, regulatory pressure was muted, and growth was rapid. But the model was always exposed. Several states had already begun passing laws restricting or banning real-money play, and a cloud of regulatory uncertainty lingered over the category.

What Indians lack in spend-depth, they make up for in product loyalty, providing much-needed liquidity to games that live and die by their multiplayer and social depth.

In mid-2023, the landscape changed sharply with the imposition of a uniform 28% goods and services tax (GST) on online gaming winnings. This triggered a sharp pullback especially with the retrospective provision to the tax. Acquisition slowed, margins thinned, and by 2024, no major RMG platform had raised fresh venture funding. Startups without deep reserves or diversified revenue streams were forced to sell or shut down, resulting in widespread consolidation. Yet the incumbents adapted swiftly and have been resilient. Platforms like Dream11, Gameskraft, Winzo, and Zupee adjusted to the new tax regime, rationalised costs, and were able to navigate business turbulence. While the overall category remains under regulatory pressure and there is an ongoing case for removal of retrospective GST in the Supreme Court of India, the RMG companies that survived the shakeout have emerged as dominant players in their respective sub-segments and have already started diversification by launching gaming studios, global M&As, and more. As of August 2025, the Government of India has introduced new legislation in the form of the Online Gaming Bill 2025. The bill draws a clear line between permitted and prohibited gaming activities. Esports and online social games are to be recognised and regulated within a formal regime, while online real money gaming is to be prohibited at the national level. To give the prohibition teeth, the bill criminalises multiple links in the value chain, with sanctions across promotion, advertising, transfer of funds, and gaming services. With the advent of new legislation, the future of real money gaming in India looks uncertain and that can potentially cause some unknown second order effects.

Many paying users in India first encountered digital spending through fantasy sports or competitive skill games. These platforms demonstrated that Indians were willing to pay for the sake of competition, stakes, and community. This play-and-pay pattern laid behavioural groundwork that continues to shape mid-core monetisation. Some platforms are already experimenting with hybrids (skill-based titles that incorporate real-money mechanics or progression systems that mimic competitive incentives). These are designed to retain engagement while avoiding regulatory scrutiny. More broadly, RMG taught Indian developers a crucial lesson: monetisation is possible when gameplay aligns with social status, habit loops, and local culture. The question now is whether those same triggers can be reactivated within fully compliant, long-term video game economies.

The investor narrative has also shifted. Studios that were previously RMG-first have expanded their strategies to include incubation and M&As of game studios with a view for near-future IPOs. Small-scale fundraising is increasingly anchored around proof-of-revenue, especially among studios able to demonstrate monetisation through in-app purchases or webshops. There’s renewed interest in service-layer businesses: publishing, analytics, and infrastructure offerings that can help local studios grow and retain users more effectively.

On the content side, some genre patterns are becoming clearer. Shooters continue to lead in domestic consumer spend, even after multiple regulatory disruptions. Titles like Battlegrounds Mobile India and Free Fire have cultivated huge followings in Tier 1 and Tier 2 India. Despite temporary bans on these in 2022–23, players migrated to alternative titles, resulting in a 37% YoY surge in in-app revenue outside of those blockbuster games. It is noteworthy that just two games have each generated over $100 million in annual revenue out of India, showcasing a willingness to spend when the price is right and value is visible. This phenomenon also inspired a slew of six to seven Indian gaming studios to develop their own mobile shooter games; an unprecedented network effect in the country.

Beyond shooters, strategy games like Clash of Clans, Evony and Whiteout Survival have built loyal followings with up to 5.7 million daily active Indian users and, in some cases, with day 30 retention metrics crossing 30%. What Indians lack in spend-depth, they make up for in product loyalty, providing much-needed liquidity to games that live and die by their multiplayer and social depth.

This is particularly true of older and higher-spending cohorts. There is also strong early traction around simulations and builders that carry a cultural or spiritual theme such as Temple Sims. These don’t always monetise well yet, but user interest is real. The wildcard is sports. Cricket as a mobile category has seen releases over the years but it appears under-monetised; we believe there are signals emerging from the hybridisation of sports with strategy and arcade formats that merit watching. Notably, a global gaming giant like KRAFTON acquiring an Indian studio Nautilus Mobile for its cricket IP “Real Cricket” shows this segment is primed for more growth.

India’s gaming story began with jugaad – the act of patching together tools, teams, and tactics to thrive – and its next chapter is about turning those instincts into systems.

Meanwhile, Roblox has begun to gain traction among young users in Tier 1 India, especially in metros where digital-native children are seeking personalised and social game experiences. While hard revenue data remains sparse, early signs point to rising MAUs and session times. This generational shift hints at a broader trend: Indian players (especially younger ones) are increasingly drawn to sandbox and UGC-led games that offer expression and agency over linear content. In parallel, a new class of Indian creators is emerging within the same global UGC ecosystems. A new crop of devs is leveraging creator-friendly tools, modular systems, and low-cost scalability to scale on platforms already embedded in Gen Z behaviour. Early winners have already emerged, with some studios crossing $20 million in UGC revenues.

Lastly, India’s monetisation rails are slowly catching up to its user scale. UPI penetration and app store alternatives have made it easier than ever to pay. Millions of users already subscribe to OTT platforms and premium content via low-cost bundles. The leap from ad-funded to subscriber-funded models is underway in adjacent sectors. Whether it will translate to games remains to be seen, but the infrastructure and behavior is now in place.

We believe Indian studios building for India will be long-term winners as the development ecosystem evolves as there will be headwinds in the short term; while India’s gaming market deepens, we expect to see more local content replace global content as it did with other media formats. While in the short term we also see live ops battle-tested teams making successful casual games for global audiences and finding winners in mobile gaming globally which startups like Gameberry and Spearmint have demonstrated.

In addition, we see that the onset of AI has democratised game development in emerging markets like India – with small teams now starting to deliver good quality game assets in a more efficient manner. As AI continues to evolve, it is increasingly becoming easier for a wider pool of creators to actualise their creative visions efficiently: a trend, which we believe will play a key role in increasing the number of global winners from India.

Similarly, in game publishing, we see AI creating opportunities for optimisation across production, live ops and analytics funnels. We see evidence of this with the rise of more games businesses focused on publishing, distribution and game analytics – a corpus of knowledge which has hitherto been gatekept by larger, more experienced mobile publishers and developers.

The post-IDFA world is still taking shape in mobile gaming, and with AI, how and what a mobile game publisher becomes is yet to be determined – but there is a clear opportunity for a large market like India to develop publishing as a moat.

We foresee that India is on track to see 5 to 6 mobile games cross the $100 million annual IAP revenue mark by the end of 2025. That would represent a significant shift from a historically ad-dominated monetisation model – one that signals the arrival of India as a true top-tier IAP market. India’s gaming story began with jugaad – the act of patching together tools, teams, and tactics to thrive – and its next chapter is about turning those instincts into systems. In an increasingly fragmented, mobile-first, voice-driven digital landscape, the next station isn't catching up to global standards – it's setting them. All aboard.

Disclaimer: None of the above should be taken as investment advice or an advertisement for investment services. Inherent in any investment is the risk of loss. For more info, visit bitkraft.vc/legal.