The US is loud right now. Not metaphorically. Actually loud. For the first time in 32 years, the FIFA World Cup is being played on American soil, and Mauricio Pochettino’s USMNT has just made it through to the Round of 16 with a win over Bosnia and Herzegovina. Belgium is next on Monday night. Bars in New York, Los Angeles and Kansas City have been packed on match nights. Resale prices for the group-stage matches reportedly cleared four figures for the cheapest seats. Pulisic jerseys are everywhere. The tournament final will be played in New Jersey on July 19.It is worth pausing on what is happening, and not just because it is fun to watch a country reintroduce itself to a sport it has spent decades treating as somebody else’s. The USMNT’s World Cup run is also a perfect, immediate case study in something much bigger: the value generated by sports is no longer flowing to the same places it used to. For most of the modern history of professional sports, the answer to "who wins when sports wins?" was simple. Owners won. Media rights holders won. A small number of marquee sponsors won. Players, communities, and fans got the experience. Owners got the value. That structure is unwinding. Not in one place, but simultaneously across three vectors. Downward, to athletes, who are now economic actors and investable brands rather than salaried employees. Outward, to fans, who are no longer spectators but active participants with money in the game. And outward again geographically, to assets and leagues outside the traditional Tier 1 Western core that have been mispriced for decades. What this means is that the sports economy is being structurally rebuilt. It also means that an unusual amount of technology infrastructure is going to need to get built to make it actually work. That is where this gets interesting.

Vector one: value flowing downward to athletes

The most visible shift is the one happening to athletes themselves. In US college sports, the 2021 NCAA decision to permit name, image, and likeness compensation reset the entire economics of amateur competition. Within four years, what was technically still amateur sport had become a market worth $1.67 billion in 2024-25 according to Opendorse, projected to exceed $2.5 billion in the first year of formal revenue sharing. Top quarterbacks and basketball players now sign collective deals worth seven figures before they ever play a professional game. Tax advisors, brand managers, and financial planners who used to wait until the NFL Draft to acquire a client now compete for relationships with high school juniors.

This is not happening in a vacuum. The next layer, formal revenue sharing between universities and their athletes, is arriving under the House v. NCAA settlement framework. Schools that participate will be paying their athletes directly, on top of NIL income, with a per-school cap of up to $21.3 million in year one. The amateur model that defined US college sports for a century is effectively over. What replaces it is something closer to professional minor leagues, with all the financial complexity that implies.

The professional side is moving in a parallel direction, just more slowly. Player shares of league revenue have ticked upward in collective bargaining agreements across the NFL, NBA, and MLB. Players increasingly own equity in companies they endorse, take board seats, and structure their careers around brand-building rather than purely athletic performance. Christian Pulisic, currently leading the USMNT through this World Cup, is a study in the same shift. He plays professionally for AC Milan, captains the US national team, and carries endorsement deals with Puma, BOSS, Michelob ULTRA, Pepsi, Gatorade, and half a dozen other consumer brands, several of them equity-linked. This World Cup alone has put him at the center of global campaigns from Rexona, Mondelēz, and Nike. He is a soccer player. He is also a small-cap investment portfolio.

The implication is that athletes have moved from being employees to being something more like founders, with revenue diversified across salary, endorsement, equity, and increasingly their own direct-to-fan platforms. The infrastructure to serve them, including financial services tailored to athlete cash flows, brand management platforms, NIL marketplaces, and tools for managing tax and compliance across multiple jurisdictions, is still being built. Almost none of it existed five years ago. Most of what exists today is undercapitalised relative to the size of the market it serves.

Vector two: value flowing outward to fans

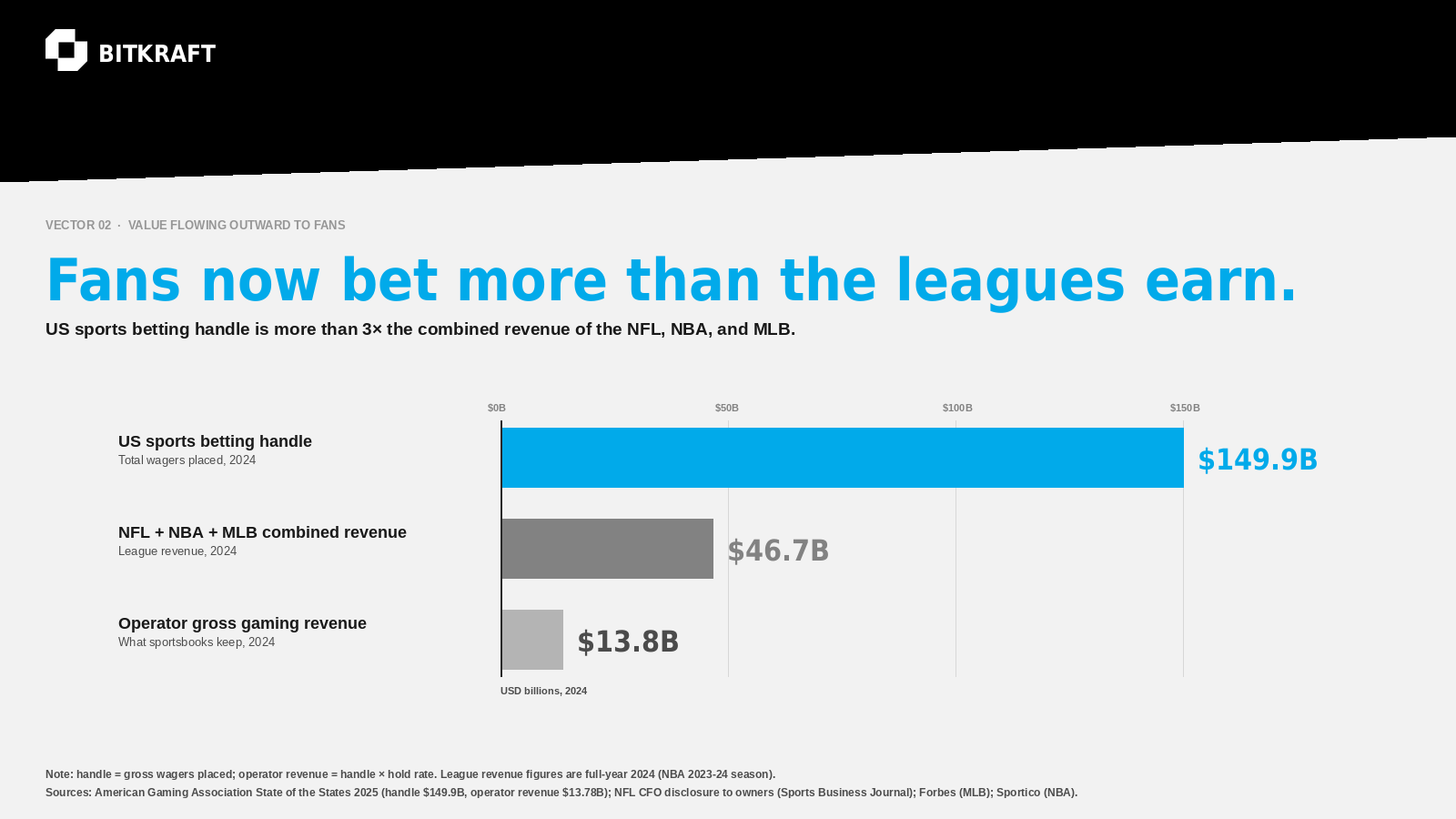

The second redistribution is happening on the demand side. US sports betting handle reached $149.9 billion in 2024 according to the American Gaming Association, with 38 states operating legal sports betting markets. The number has continued to climb. These are not marginal numbers. They are more than three times the combined revenue of the NFL, NBA, and MLB.

What betting has done is convert a passive viewing experience into an active financial one. Tens of millions of fans now have skin in the game in a literal sense. The relationship between fan and sport is no longer mediated only by emotional investment. It is also mediated by a real, measurable financial position that updates in real time. The behavioural shifts this produces, including longer viewing sessions, deeper engagement with secondary leagues, and a willingness to follow sports the fan has no cultural connection to, are significant and durable.

The next layer is arriving in prediction markets. Platforms like Kalshi and Polymarket have moved from the margins to the mainstream of financial media coverage. The regulatory landscape remains contested in the US and varies across European jurisdictions, but the underlying behaviour is clear. Fans are increasingly comfortable taking financial positions on outcomes of all kinds, sports outcomes among them. The line between betting, prediction markets, and traditional financial speculation is thinning.

This piece does not take a position on whether the broader expansion of betting and prediction markets is socially desirable. Reasonable people disagree, and the regulatory environment will continue to evolve. What is harder to dispute is that this represents a structural redistribution of where the value generated by sports accrues. A meaningful share of it now sits with the operators of betting and prediction infrastructure, with the data providers who power them, and with the fans themselves when their positions pay out. That money used to flow somewhere else.

Vector three: value flowing outward geographically

The third vector is the one most easily underestimated. The most undervalued assets in global sports are not in the NBA or the NFL or the English Premier League. They are in the leagues and clubs and properties that have not yet been discovered, or that have been systematically underpriced because the global media machine has not pointed at them yet.

The clearest case study is Wrexham. When Ryan Reynolds and Rob McElhenney acquired the Welsh fifth-tier football club in February 2021 for roughly £2 million, it was a romantic acquisition with no obvious financial logic. Five years later, after three consecutive promotions, a Disney+ documentary that became a global cultural property, and a fan base that grew from a few thousand in Wrexham itself to a meaningful international following, the club is valued at £350 million as of late 2025 according to Bloomberg reporting on the Apollo Sports Capital minority investment. The valuation uplift is not the point. The point is the mechanism. Reynolds and McElhenney did not just buy a football club. They bought a piece of distressed media IP, attached a compelling narrative, married it to operational discipline on the football side, and used the platforms now available to anyone — streaming, social, direct-to-fan content — to compound the value far faster than the underlying sport alone would have allowed.

That playbook is now being run, with varying degrees of competence, across European football. Tier 2 and Tier 3 acquisitions that would have been afterthoughts five years ago are now competitive processes with multiple credible bidders. Women’s football has gone through a similar revaluation. NWSL club valuations have risen dramatically, with the average franchise now worth $184 million per Sportico’s 2026 valuations, up 179 percent since 2023. Angel City FC leads at $335 million; several other clubs trade above $200 million. The Women’s Super League in England has gone through an analogous compression of the valuation gap with men’s football. Rugby is starting to show similar dynamics in selected markets. Cricket, particularly franchise cricket outside the Indian Premier League, has become an investable category in a way it was not a decade ago.

The pattern is consistent. Undervalued sports assets, when they meet operational competence and modern distribution, can produce non-linear value creation that traditional sports investing models simply did not contemplate. The question is no longer whether the Wrexham playbook is repeatable. It is being repeated. The question is which assets, in which sports, in which geographies, are still mispriced, and what infrastructure does an investor need to identify them and execute on them.

The infrastructure gap

Three vectors of redistribution, all happening simultaneously, all structurally durable. The question for a technology investor is where the infrastructure layer is. The honest answer is that it is mostly nascent. Athlete financial services, NIL marketplaces, and brand management tools are early. Prediction market infrastructure is contested regulatorily and commercially. International ticketing platforms remain fragmented and underbuilt. Streaming infrastructure for non-Tier-1 sports is uneven. Sports data and analytics for leagues outside the NBA, NFL, and Premier League are far behind what those Tier 1 properties enjoy. Direct-to-fan engagement platforms that work across sports, geographies, and content types are still being figured out.

This is not a complaint. It is a description of where the opportunity is. When a sector undergoes structural value redistribution at this scale, the infrastructure that serves the new structure tends to be built by a new generation of operators, not by the incumbents whose business models were optimised for the old one. The big sports data companies, the legacy media rights holders, and the traditional team-ownership structures are not going to build what the new sports economy needs. Some of them will buy it after the fact. The category-defining companies will be built by founders who understand both the sport itself and the technology layer underneath it.

Why BITKRAFT is paying attention

We have not historically been a traditional sports tech investor. Our roots are in esports and competitive gaming. The thesis that has driven the firm for the past decade is that interactive entertainment, broadly defined, is one of the most important consumer categories of this generation. Sports has been adjacent rather than central.

That is shifting. Our investment in Snow League, a public investment we have spoken about previously, reflects what we think is the more interesting version of how a fund like ours can engage with sports. Snow League is not a bet on traditional broadcast economics. It is a bet on a new property at the intersection of culture, engagement mechanics, and an underserved fandom that no incumbent league has structured itself to capture. A separate dedicated piece on Snow League is coming. The point worth making here is that the framing matters. We are not going to be the firm writing checks to the next majority owner of an established Tier 1 franchise. That is not our edge. We are interested in what gets built around and underneath the new sports economy, the infrastructure, platforms and properties that make the next generation of fan engagement, athlete economics, and league formation actually work. Sports might be a category for us. Not in the way it has been for traditional sports tech funds, but in a way that connects to how we have always thought about interactive entertainment, community, and the technology layer that holds those experiences together. The redistribution of value across the sports economy is creating exactly the kind of structural opening that interests us, and the operators we want to back are increasingly emerging from the spaces where the new economics and the new technology meet.

What is happening in the US right now is a reminder of why. A country of 340 million people, briefly wrapped up in a tournament it has spent decades treating as somebody else’s sport, with all the cultural and economic and emotional weight that comes with it. Sports does that in a way nothing else does.

The interesting question for the next decade is not whether that energy continues. It will.

The interesting question is where the value goes when it does. The answer is: nearly everywhere except where it used to go. ⚽