Introduction

A young man was trekking through the jungles of Brunei, a small equatorial country on the coast of Borneo that is home to over 19 species of bamboo. While resting under the shade of a dense bamboo forest during one of these treks, a local guide explained a fascinating fact: “Did you know that while bamboo takes years to sprout, once they do, they grow up to 3 feet in a single day?” The guide explained why this was possible: The lifecycle of a bamboo plant first begins with the building of a deep and densely interconnected network of roots. This is what provides the bamboo plant a solid foundation of strength and stability, upon which the bamboo is able to grow stably and rapidly from later on.

Asia did not emerge overnight as bamboo did, but just as bamboo's strength lies in its interconnected root system, the region’s strength lies in its tapestry of interconnected cultural and technological fabric which has been woven over the decades that has catalysed the birth and subsequent meteoric rise of some of the most prominent gaming giants like Krafton, Netease, and Bandai Namc. It is a region which has laid the foundational cornerstones of new genres, gameplay systems, and monetization design which have become globally embraced and adopted into the zeitgeist of games in our generation, highlighting the ability of the region to innovate not only for the region, but on a global scale as well.

Similar to how nature enthusiasts are drawn to a bamboo forest, it should come to no surprise as well that investors are increasingly curious about and investing into Asia gaming. According to a recent report by our friends at Konvoy Ventures, Asia accounted for ~50% of global gaming VC deal value and ~49% of deal volume in 1H2023 itself quantifying investors’ desires to invest into the region as more investors are drawn by the region’s sheer scale, sustained growth, and promises of more wonders yet to be discovered.

Yet investing into Asia is no walk in the (bamboo) park. Just like how understanding bamboo requires a deeper look beneath the soil, being an effective investor in Asia requires an equally deep appreciation of local context, nuances of a ethnically diverse yet culturally similar user base, and an ability to dig deep into the underlying ecosystem and mesh of interconnected industry players, developers, and gamers. For those equipped with this highly localised contextual understanding, and who possess the will to dig even deeper, we believe the potential for outsized rewards and investment outcomes is immense.

That is why BITKRAFT recently hired Jin Oh, based out of Korea, and Jonathan Huang, based out of Singapore, to be the firm’s boots on the ground in the region to look for the most promising startups. Having spent most of their gaming careers over the past 1-2 decades in Asia, they possess broad networks, deep cultural and contextual knowledge, and unwavering passions in gaming. BITKRAFT is excited to be investing into Asia, and here is our thesis.

Executive Summary

In this section we distil the essence of our thesis into an accessible and bite-sized read that provides a 30,000 feet overview of the full discourse, the latter of which goes into far greater detail and nuance for those with the curiosity and more importantly, time, to dive deeper.

The BITKRAFT Asia Investment thesis can be broadly divided into 4 key pillars:

- Mobile-Native Cross Platform Games

- Focusing on Core Genres

- Asia as a Bastion of Web3 Gaming Innovation

- Platforms, Infrastructure, and Applied Game Mechanics

Mobile-Native Cross Platform Games: We are excited about games that are built with the mobile in mind and possess cross-play capability with PCs and Consoles. Mobile gaming continues to be a cultural touchstone in Asia, and the confluence of several secular trends including i) technological advancements and expansion of smartphones and corresponding storage sizes to ii) enable the consumption of increasingly larger games, as well as iii) the advent of cloud gaming solutions which completely remove compute bottlenecks inherent within smartphones, to engender a future where mobile gamers are able to access larger, AAA-esque titles with their peers on other platforms.

Focusing on Core Genres: We are excited about games that are midcore to hardcore in genre. Casual continues to face the greatest competition in the form of challenging economics (e.g. IDFA), lack of product differentiation (e.g. Highly similar game loops), and risk of disruption (e.g. Potential to leverage GenAI to rapidly build low fidelity games), there is also a clear trend of our younger generations preferring core to casual genres which is elaborated in time-series data in the fuller memo. Congruent to our earlier thesis of phones becoming increasingly capable of servicing larger AAA-esque games then is the corollary that gamers will consume more expansive and larger-scale titles as their devices increasingly possess the capability to do so.

Asia as a Bastion of Web3 Gaming Innovation: A thesis which deserves an entire write-up on its own, we highlight the conduciveness of Asia as a hotbed for web3 gaming innovation and why we are excited to be hunting in her grounds. Asia’ possesses all 3 key pillars which are critical to the development and eventual success of web3 gaming: Friendly crypto regulation (Government), a deep track record of technology and gaming monetisation innovation (Companies), and one of the highest crypto-adoption rates globally (Users). The openness and willingness to adopt and experiment with crypto across end users, companies, and governments is a unique and potent dynamic that is not as prevalent anywhere else in the world, and gives us conviction that more web3 gaming innovations and success stories will emerge from the region.

Platforms, Infrastructure, and Applied Game Mechanics: There are no lack of picks and shovels in Asia’s gaming startup scene, the latest and greatest of which we have sought to map out in the section below. What is worth highlighting here is the velocity at which Asia has traditionally been able to capture new paradigm shifts and produce regional solutions but is today increasingly ideating and producing for a global audience, and we are already seeing proofpoints that Asia-based gaming platforms and infrastructure can stand toe-to-toe versus its western competitors and hold centre stage on a global scale. Part of the infrastructure thesis also includes a continuation of BITKRAFT’s earlier work done on Applied Game Mechanics which revolves around product gamification, a dynamic which manifests itself in a wide variety of applications given the highly gaming-native nature of the populace. We are optimistic that we will continue to see Asia redefine the rules of gamification and drive innovation in this area.

Asia’s Growing Influence as A Global Gaming Hub

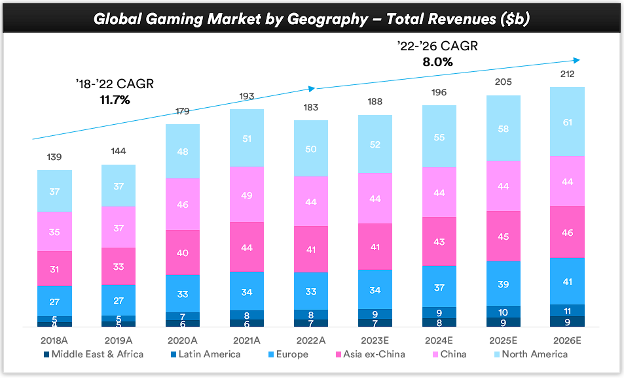

The sheer size of Asia as a gaming region is unmistakable - Newzoo estimates that Asia contributes to a remarkable 46% of global gaming revenues in 2022 and home to 2.4b gamers accounting for over 75% of the world’s gaming population today. Whilst income levels in Asia, especially Emerging Markets (“EM”) Asia, are markedly lower than gamers from Developed Markets (“DM”) in the West, the user base contribution dominance is a strong proxy and powerful macroeconomic trend that hints at the potential for the region’s growing influence and importance in the world over the mid to long-term.

Source: Newzoo Global Gamers Report 2023

As aggregate wealth continues to increase in Asia, it follows that Asia’s young, massive, and digitally-native user base will also increasingly possess greater disposable income to play and pay for games. It is a similar pattern to how other developed markets have gone through the same structural evolution in the West, and we expect this to play out in Asia as well.

Investment Thesis I: A Mobile-Native, Cross-Platform Future

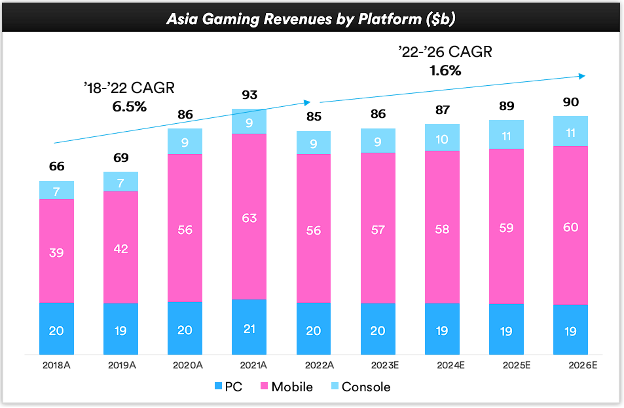

Just like how the biodiversity of flora and fauna in the West is vastly different from that in the East due to factors such as temperature and altitude, the complexion of Asia’s gaming users are also incredibly distinct compared to US/ Europe. One key reason is the hardware format through which many Asian users, especially those in EM Asia, were on-boarded into gaming: mobile.

Source: Newzoo Global Gamers Report 2023

The key debate here is whether Asian gamers will i) Transition to costlier PC/ Consoles once they acquire sufficient wealth, OR ii) Continue to play on Mobile despite being sufficiently affluent to purchase PC/ Console. We believe the answer is the latter, and here is why:

Change is The Only Constant, But Constancy Is Human Nature

Humans are hardwired to resist change, a fundamental anthropomorphic truism which we see play out often in many different areas of technology. Consider that banking used to be an incredibly physical endeavour where transactions were conducted in brick-and-mortar branches in person, until eventually a paradigm shift occurred with the advent of online banking through PCs and mobile apps.

In Asia, we saw this leapfrogging of the traditional banking experience as many emerging countries lacked the infrastructure and network of bank branches and ATMs, which funnelled and onboarded significant unbanked populations first onto banking via mobile banking apps.

Today, younger generations access banking services primarily through mobile devices despite physical stores offering more comprehensive solutions, while bank branches are often filled with older folks who prefer the traditional way of banking: because that was how they were onboarded onto banking, and humans are resistant to change.

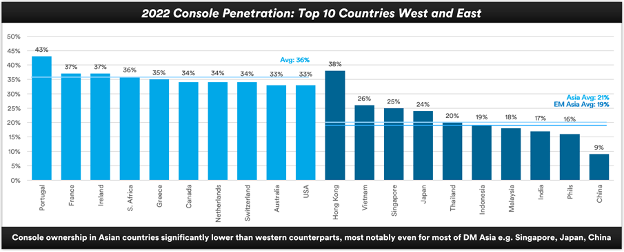

A similar dichotomy can be observed in Asia - in this region, the first tidal wave of gamers were onboarded into gaming primarily through PC/ Console experiences: these include the launch of the Playstation in 1994 and later on the proliferation of “PC Bangs” in South Korea in tandem with the launch of StarCraft, just to name a few examples. These cohorts of PC/ Console gamers are ~30 years and older now and similar to our banking example, will continue to favour PC/ Console as their primary gaming device. We see the chart above showing PC/ Console revenues staying stable at ~$30b/ year over the next 5 years as quantification of this trend.

The second tidal wave of gamers in Asia, particularly in EM Asia, have been on-boarded onto video games through the advent of the smartphone, and have have grown accustomed to the accessibility, convenience, and growing capabilities of mobile gaming. Though PC/ Console may offer more expansive experiences than the mobile, we believe these gamers will likely to remain attached to the smartphone they started with, just as the mobile banking user might prefer their smartphone over a brick and mortar store.

Source: YouGov survey as of May 2022

This hypothesis is already playing out in DM Asia, which is quantified in the data above: despite possessing the wealth to acquire PC/ Consoles, console penetration of DM asia countries remain low and mobile remains the dominant form of gaming across these markets, indicating that consumer habits and preferences are equally as, if not more important, than disposable income in deciding gamers’ primary gaming format.

Two other secular trends underpin our belief that the Asia gaming market will likely be one that remains on mobile:

Size Matters: Mobile Phones & Games Are Getting Bigger and Better

Over the past decade we continue to see an ongoing premiumisation of smartphones in tandem with ongoing increases in file sizes for mobile games. The absolute storage capacity of a smartphone has traditionally been a bottleneck for users trying to access larger sized mobile games, but that barrier is continually lowering to allow gamers to access more expansive experiences.

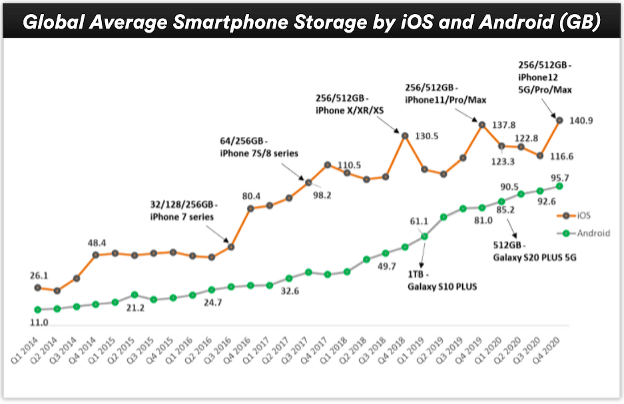

Source: Counterpoint Research, March 2021

According to Counterpoint Research, Asia continues to be predominantly an Android-based mobile market, we believe primarily due to the wide range of budget options available to EM gamers. The same research also shows that the absolute average storage size of an Android smartphone has grown 8.7x from 2014 - 2020, increasing from ~11GB to ~96GB over the same period. We expect this trend to continue and expect larger minimum as well as maximum phone storage sizes across all smartphones.

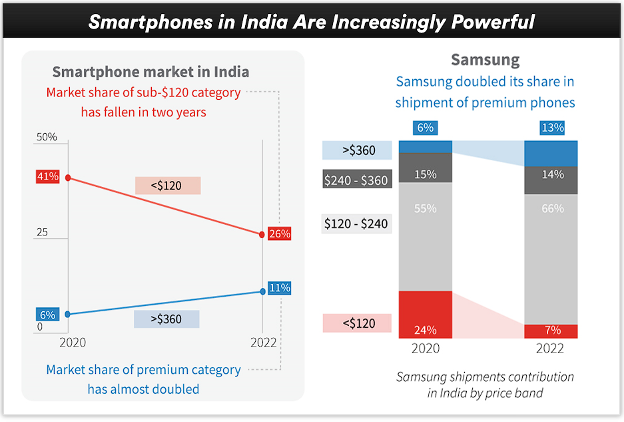

A good case study of the above trend playing out is in India, where there has been a clear increase in market share of premium smartphones (>$360/ phone) at the expense of budget options (<$120/ phone). One of these mobile brands, Samsung, has been winning total mobile market share in India by focusing premium smartphones for the burgeoning middle class when other brands had pursued a budget phone strategy.

Source: Counterpoint Research, Oct 2022

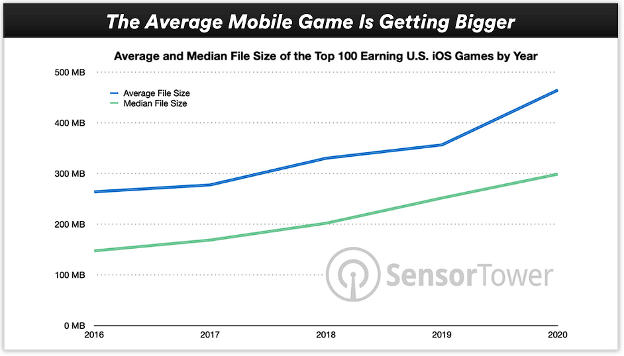

Mobile games are getting bigger as well, as illustrated in the chart from SensorTower below - As smartphone storage continues to increase, developers are increasingly making larger and more premium “AAA”-esque looking games to offer greater entertainment experiences. Not only are average file sizes increasing, the biggest games are also getting bigger: PUBG Mobile, launched in 2017, requires between 4-8GB of storage for a full download, while Genshin Impact, launched in 2020, requires over 20GB for a full download, not to mention a powerful and snappy CPU to ensure a smooth and seamless experience.

Source: SensorTower, March 2021

Additionally, the ongoing proliferation of cloud gaming will further lower the barriers of entry to accessing premium mobile titles by eliminating the need for a premium smartphone completely. By allowing users to rent GPUs in the cloud, gamers will be able to harness the compute power of the latest and greatest chips in the world, and stream the biggest video games onto the most budget of phones.

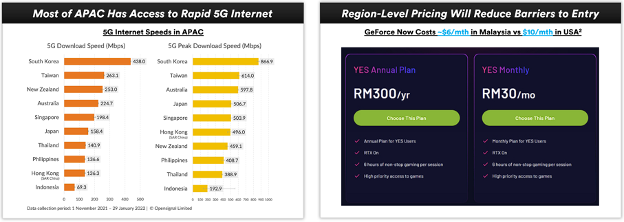

Source: OpenSignal, GeForce Now Malaysia Website

The necessary foundational infrastructure required for cloud gaming to achieve escape velocity in Asia are now in place: Rapid internet access across the region and tailored region-level pricing to allow less affluent EM users to access cloud gaming solutions. From our work on the ground we are already starting to hear vendors exploring selling cloud gaming services for as low as $2/ mth. We believe this will potentially cultivate an unlock opportunity to further accelerate gaming consumption as Asian gamers will now be able to play even the most demanding AAA titles on their mobile devices and even stream it onto their TVs, eliminating the need for consoles and further entrenching their mobile-native behaviour.

The Case for Cross-Platform Gaming

The above segment lays out the case for mobile as a dominant device in Asia for gaming, but saying our investment focus will be mobile games is only partly true. Crucially, we are looking for games conceived with the finesse of mobile-centric design, but also allow for cross-play with gamers on other platforms including PC and Console.

Mobile gaming remains a cultural touchstone in Asia but our investment horizon is global - It is one thing to ride the tidal wave of mobile gaming but another to harness its tidal force and merge different oceans and bring different gamers into a shared universe. In investment speak, mobile-native cross platform games hence address a global TAM that spans the PC/ Console dominant markets in the West as well as the vast mobile user base here in the East, in turn maximising monetisation potential and providing an unfair edge against those which do not.

We are starting to see greenshots of this thesis as there is a clear trend of such mobile-native cross platform games emerging: Genshin Impact, Diablo Immortal, Honkai: Star Rail, Albion Online, and Pokemon Unite, just to name a few. As mobile’s ubiquity continues to deepen not in Asia but across the youth globally, a core investment thesis of ours therefore focuses on hunting for the next genre-defining game that is built with this channel distribution in mind.

Investment Thesis II: Focusing on Asia Core Genre Studios

Having initiated our discourse with a reference to bamboo, it is only fitting that we once again draw inspiration from the forests - In a quiet village in ancient China, a musician creates soulful melodies with a bamboo flute. The melody is simple, raw, and pure: easily understood and appreciated, but also replicated. As we teleport to the bustling cultural hub of Beijing, the music evolves: we enter the grand stage of the Beijing Opera, where a fusion of instruments, vocals, and performances come together, creating a multi-sensory experience that's rich, complex, and deeply immersive.

This progression, from the simplicity of the bamboo flute to the intricate tapestry of the Beijing Opera, mirrors our view on Asia's gaming industry

Casual mobile games are the bamboo flutes of the digital realm – straightforward, universally appealing, but with a depth that might be limited in its reach in enchanting consumers. Their soothing melodies may charm for a while, but might lack enduring resonance. In contrast, core mobile genres resonate with the Beiing Opera's intricacy - they offer a kaleidoscope of experiences, intricate challenges, and narratives that keep players deeply engrossed, much like an audience enchanted by a night at the opera. Make no mistake, there will always be room for tranquil bamboo flute solos, but there's also a clear and unmistakable craving for the grandeur of the opera.

At BITKRAFT, our investing strategy recognizes this nuance. We are not merely investing in fleeting tunes, but in experiences that will hopefully be as memorable and eternal as the biggest musical productions of humankind. And this is the core tenet of our 2nd investment thesis: Focusing on core genres

Skating To Where The Puck is Going

Source: data.ai State of Mobile Gaming 2023

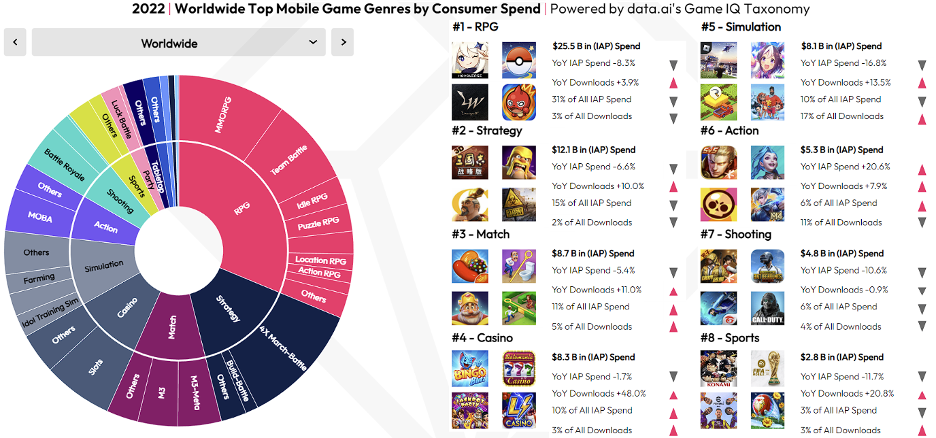

In data.ai’s State of Mobile Gaming 2023 report, we noticed a few interesting insights that hinted at the direction in which the market was going. Starting with the lay of the land, we noticed that midcore/ hardcore (“Core”) genres accounted for over 62% of the total market, comprising several key categories including RPG, Strategy, Action, and Shooting games. The remaining 38% was accounted for by hypercasual/ casual genres, including Match 3, Casino, and a longer tail of niche genres.

The next interesting chart from the same report is the following one which breaks down gamers by age group and ranks their most preferred to least preferred genres. For brevity we are only showing the chart for US, but a review of the same data for Asia countries reveal remarkably similar trends:

The youth of today are the spending adults of tomorrow, and the data shows a clear gravitation of the gamers aged 18-24 towards mid to hardcore genres such as Battle Royale, FPS, MOBA, and Strategy, whilst showing muted interest in casual genres such as Match 3, Puzzle games, and Slots/ Gambling. The reverse is true for the oldest segment of the gaming population aged 45+, which sees an incredibly high affinity for casual genres and little to none for core genres.

The other interesting trend that one may delineate from these charts is that the cohorts of gamers aged 25-34 (pink dots) and 35-44 (red dots) respectively seem to have fairly similar preferences for games (pink and red dots are quite close to each other).

The implications are twofold - First, we notice that there remains strong demand for core genres when youths age into that demographic, and it will not be till when they are 45 before they acquire a taste for casual games, if at all. Second, whilst there is indeed some adoption of casual games amongst these two demographics, age does not seem to be the underlying reason since we see those aged 25-34 playing as much casual games than those aged 35-44.

This gives us comfort against the counterargument gamers will eventually migrate onto casual genres when they age. In fact, the data suggests we will continue to see strong demand for core games as the youngest cohort ages.

Finally, consider the sheer incremental TAM that is being added to the core genre TAM over the long-term if our thesis plays out: Today, Newzoo estimates global mobile gaming to be a $92b market growing to $101b by 2026E. Core genres contribute ~62% or $57b of the market today, but should it grow to 75-80% in the next 5 years, its corresponding market size swells to a range of $76b - $81b, representing a 33-42% growth in the absolute TAM of core genres.

These charts paint a clear direction of where the puck is going, and therefore where we will be skating towards as well.

Asia’s Potential Home Ground Advantage

The proverbial bridge connecting our i) Mobile-native cross-platform thesis with that of our ii) Focus on core genres brings us back to our homeground Asia, which we think is well-positioned to win in such a future.

Source: Newzoo Global Gamer Study 2022

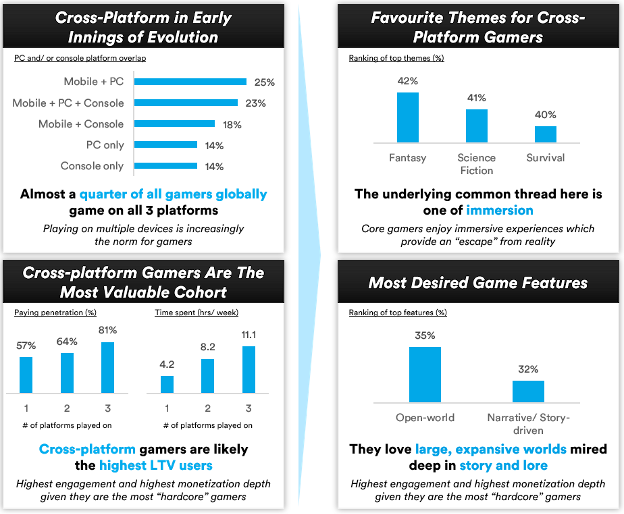

Not only are cross-platform gamers the highest LTV users, they also exhibit an inclination towards core genres, specifically those with open-world and narrative-driven gameplay. It should come as no surprise to our readers that Asia is a powerhouse and trailblazer of producing these genres. A look at the genres of the most successful mobile games here in Asia paints a clear picture:

Source: data.ai State of Mobile Gaming 2023

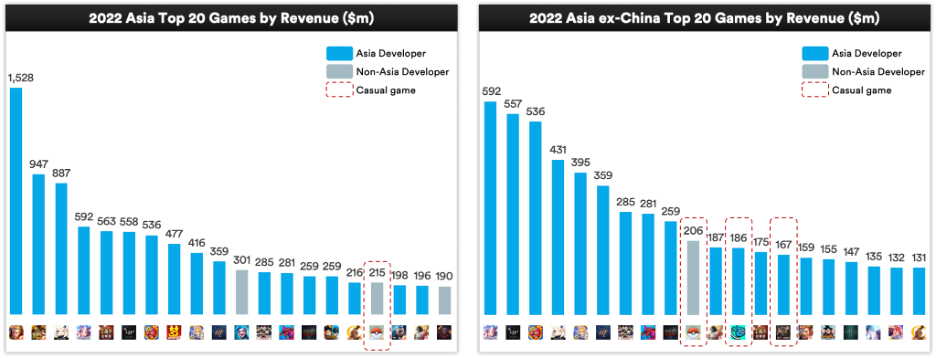

Across Asia, 17 out of the top 20 games in Asia are in the core genres including MMO, MOBA, Open-World, FPS. Knowing that China accounts for about half of the entire Asian gaming market, we stripped out China to assess if a single country was swinging the entire data set, but the picture remains unchanged: 19 out of the top 20 games in Asia ex-China are core genres.

It is also noteworthy that a staggering majority of these games are developed by Asian developers, with only a minority of games such as Pokemon Go and Wild Rift coming from Western developers. In other words, investing in Asian mobile studios provide an outsized possibility of successfully addressing the largest mobile gaming market in the world.

Finally, it is also worth highlighting that charts showing top grossing games do not show the associated costs required to produce as well as maintain the live-ops for these titles. This is an important nuance as these blockbuster hits require corresponding blockbuster budgets, and therefore not suitable for the VC funding model. The advent of AI however is upending the cost structure of video game production by allowing studios to produce significantly more with significantly less, and in turn rendering these models far more appealing and suitable for VC funding than ever.

Continent of Dark Horses

One prevalent viewpoint amongst gaming investors is the emphasis on backing founders with extensive experience from well-established game studios. These founders, with their deep operational experience and established track record, possess a clear competitive advantage against newer, emerging founders. BITKRAFT does not shy away from backing storied founders with genre-defining ideas, but that is not the only weapon in our toolkit. Most importantly, as we study the vibrant tapestry of Asia's gaming ecosystem, a different narrative challenging this dominant paradigm has played out.

In Asia, there appears to be a persistent pattern of founders with non-pedigree backgrounds pioneering some of the most iconic games that have graced the global stage. Consider Dungeon Fighter Online, a multiplayer beat-em-up role playing game that was developed by Neople back in 2005 that has gone on to generate over $22b in lifetime revenues. While Neople is a wholly-owned subsidiary of NEXON, i) Neither Neople nor NEXON were considered gaming giants back in 2005, and ii) Neople’s prior experience was primarily in casual games, yet went on to produce an action beat-em-up that has become one of the highest-grossing franchises of all time.

Consider also the story of MiHoYo, whose founders met as computer science students back in Shanghai Jiao Tong University and went on to establish their own studio without having spent a single day in any gaming company, nor raised any funding from investors. MiHoYo’s philosophy is to create “Something New, Something Exciting, and Something Out of Imagination'', which was likely to be the underpinnings of the genesis of Genshin Impact. Today, Genshin Impact is estimated to generate ~$2b of revenue a year, while MiHoYo itself has grown to over 5,000 employees globally, in search for the next game that is Something New, Something Exciting, and Something Out of Imagination.

The examples are numerous and the unifying thread is clear: Heralds in gaming do not only emerge from the gilded halls of storied gaming giants, they often also emerge from the most inconspicuous places. Non-traditional founders, armed with a tabula rasa uncoloured by the brush of industry dogma, are often the fringe thinkers who are unburdened by legacy and unrestrained to reimagine and drive new paradigm shifts in gaming. Venture is all about backing “the crazies, the misfits, and the rebels” who are bold enough to change the world, and it will be these founders whom we will always be on the hunt for.

It will not be easy to find these founders, but where sourcing and information asymmetry exists, investors with boots on the ground and possess the will to hunt will find the greatest outsized outcomes there.

Potential Gap in Funding Value Chain

A key reason for BITKRAFT’s expansion into Asia is the leadership’s observation of a catalyst at the capital markets layer that presents an opportunity for gaming venture capital.

As the gaming giants in Asia continue to grow and scale, they will increasingly come face to face with the Innovator’s Dilemma, where large incumbents tend to focus on the core to ensure stable and predictive cashflow and reduce investing into and/ or incubating new disruptive ideas. This is a natural progression for most companies as they scale and explains why disruption often emerges from smaller-scale startups.

This tectonic shift in the early-stage landscape for studios in the region is a regime change, and with regime changes emerge investment opportunities. As early-stage investors focused on the Pre-Seed to Series A rounds, we believe BITKRAFT is well-positioned to fill the funding gap for early-stage companies and serve as the discovery mechanism of disruptive new startups.

Investment Thesis III: Asia As A Bastion of Web3 Gaming Innovation

Right Place, Right Time

No discussion of gaming is complete without a discourse on web3, a subject which continues to excite us here in Asia. Just like bamboo, this digital transformation has begun to take root in a region where soil is fertile and conducive for the proliferation of an extensive root system, which will provide strong anchors for bamboo’s eventual emergence.

Web3 gaming sits at the intersection of both web2 gaming and blockchain technology, so before we double-click into the middle of the venn diagram, we take a look at its two underpinning pillars.

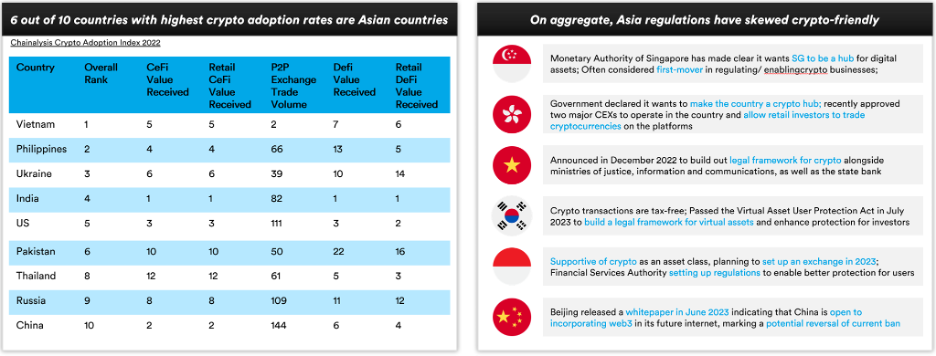

An assessment of the current state of adoption and government attitudes for cryptocurrencies in general paints a highly complementary picture. Crypto sees high adoption especially in EM globally due to many reasons e.g. promise of financial democratization, lower cost and higher speed remittances etc. In Asia, this is further amplified by crypto-friendly regulations for enterprises, enabling a virtuous onboarding cycle for consumers and enterprises alike.

Source: Chainalysis, BITKRAFT research

Within gaming itself, it is important to highlight the region’s innovative culture towards novel monetisation mechanics and more importantly, gamers’ reception to being monetised in new ways. Asia has a rich heritage in embracing and seeding new tech that have transformed gaming, and a good example of this progressivism can be found in South Korea’s role in free-to-play games. Students of gaming history would know that the concept of free-to-play originated from South Korea in the form of Nexon’s KartRider: the game was widely recognised as the first “freemium” game launched all the way back in 2004 which eventually trailblazed the way for the advent for F2P games that monetised via in-app purchases.

Another good example is GREE’s Dragon Collection, a trading card game which launched in Japan in 2010 that quickly gained the reputation as a “gacha” game, a sardonic abbreviation of Japan’s “gachapon” or capsule vending machines which are culturally pervasive in Japan. Dragon Collection is often regarded as the world’s first gacha or “lootbox” mechanic driven game and by late 2010, had over 10m cumulative users at the same time when Gree and DeNa were accounting their SNS Community to comprise of 20-30m users, testament to the pervasiveness of the game.

It is important to note not only the openness to innovate on monetisation design, but also the receptiveness of gamers to these novel mechanics that is a core underpinning for our excitement of web3 games in Asia. It is hence not surprising that the west has generally responded allergically to the first iteration of web3 games whilst it was received with far less scepticism in Asia, and in turn explains why we continue to see web3 gaming startups emerge in this region despite the underperformance of the broader crypto market.

A good interview which encapsulates the nature of game development in the East vs West was done by Jeff Lyndon back in 2015, where Jeff opines that Western developers tend to focus on developing novel/ fun/ enjoyable core experiences, whilst Chinese developers (as a loose proxy for rest of Asia) tend to focus on developing new monetisation systems, and then layer that onto whatever is the most popular Western experience out there at that time.

A good recent example of this dynamic playing out could be observed in the case of Vampire Survivors, a 2D roguelike launched in Dec 2021 which won the prestigious Best Game at BAFTA Awards in 2023, beating out heavyweights like Elden Ring and God of War. The game was launched only on Steam and sold between $3-5 per unit, achieving lifetime sales of ~6.5m units and lifetime revenues in the range of $20m-33m. Shortly after, Singapore-based mobile studio Habby launched Survivor.io, a 2D roguelike F2P title that monetises via typical mobile monetisation mechanics. The game went on to generate over $200m since launching in August 2022, almost 10x that of what Vampire Survivors has made, despite both titles having similar gameplay characteristics and differing primarily in monetisation design.

Web3 games inherently require a balance of both strong monetisation design and gameplay, we believe Asia continues to be well-positioned to seek out founders who are equipped with deep skillsets in both.

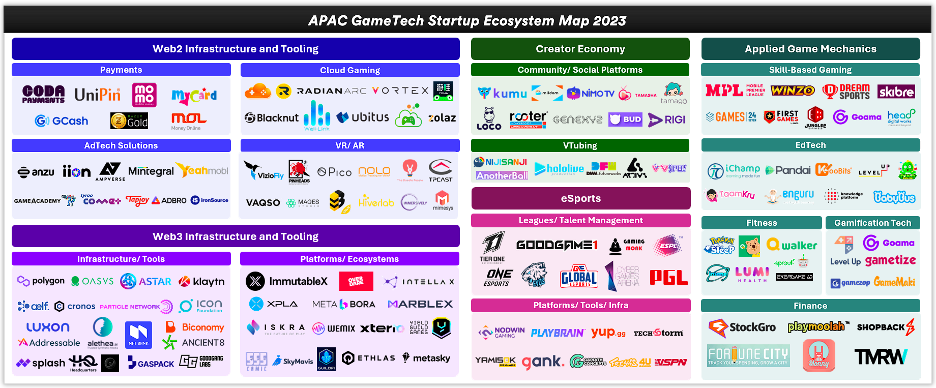

Investment Thesis IV: Platforms, Infrastructure, and Applied Game Mechanics

The preceding sections have revolved entirely around our content investment strategy, which is only one of 3 pillars within BITKRAFT’s Global Investment Thesis. In the following and final section, we explore the vibrancy of Asia’s non-content startup ecosystem and where we expect to find opportunities to invest.

Source: BITKRAFT research

Infrastructure and Tooling

Asia possesses a tremendous breadth and depth of opportunities in the gaming infrastructure space with each sub-genre warranting an entire thesis of its own which we could not reasonably include within this Asia piece, but there are key underlying themes worth highlighting.

Track record of swiftly capturing new paradigm shifts

Asia has traditionally and repeatedly caught on very quickly as well as also built for new shifts in gaming, on par with if not faster than the West. A good example of this is the web3 gaming platform space, where most if not all of the contemporary leading platforms have been founded in Asia e.g. Immutable X from Australia, Overdare or Intella X from South Korea. Another good example is cloud gaming, which has a rapidly growing ecosystem of startups building on a secular tailwind that we believe will expand the overall gaming TAM e.g. Ubitus from Japan, Radian Arc from Australia.

Another interesting example, albeit not entirely gaming related but still speaks to the region’s ability to scale tech solutions, is the story of short-form video apps in India. When India banned Tiktok in June 2020, a whole slew of short-form video apps (e.g. Moj, Josh, DailyHunt, MX Takatak) launched within the next 6 months, the fastest of which launched within 4 days post-ban, and by the end of the year there were at least 10 different competitors within the space, testament not only to the technical ability of India businesses but also their entrepreneurial acumen.

From Regional to Global

A deep and technically savvy talent base across Asia positions the region well to incrementally iterate on existing solutions and produce them a more localised and regional populace, but more importantly, continue making zero-to-one innovations mentioned in the earlier examples such as web3 and cloud gaming, amongst others.

While we are excited by the prospects of both, we are particularly excited about Asia’s ability to transition from copycatting global solutions for regional markets into producing solutions for a global audience.

Delineating the Cyclical from the Structural

Whilst the growth of infrastructure opportunities in Asia is a clear structural theme, we remain cautious about the cyclical nature of capital crowding into the “picks and shovels” as markets over the last twelve months continue to be in a risk-off mode, driving up valuations of infrastructure assets and deteriorating its risk-reward profiles. This, coupled with the fact that infrastructure and tooling businesses often start off fragmented and over time consolidate into a few leading players, implies we have to maintain discipline when evaluating and investing into infrastructure opportunities.

Applied Gaming Mechanics Hub

At BITKRAFT, we believe gamification is a thing of the past and has evolved into something more sophisticated, what we call Applied Game Mechanics (or “AGM” for short). Whereas gamification was primarily about turning existing products into games, AGM is about building products that subtly incorporate the most effective game design principles and mechanics from the ground up. Our earlier work and thesis around AGM is published here, which we highly recommend reading before diving into the next segment here which builds on our earlier work.

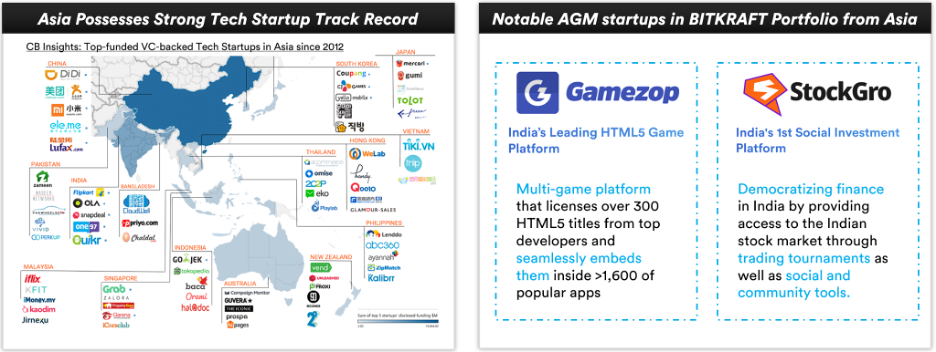

AGM businesses inherently require a good balance of technological + gamification design capabilities, and it is the region’s vibrant and deep engineering expertise that adds to its viability as an AGM hub. Consider the map below, which highlights the most well-funded, VC-backed, tech startups in Asia since 2012.

Source: CBInsights

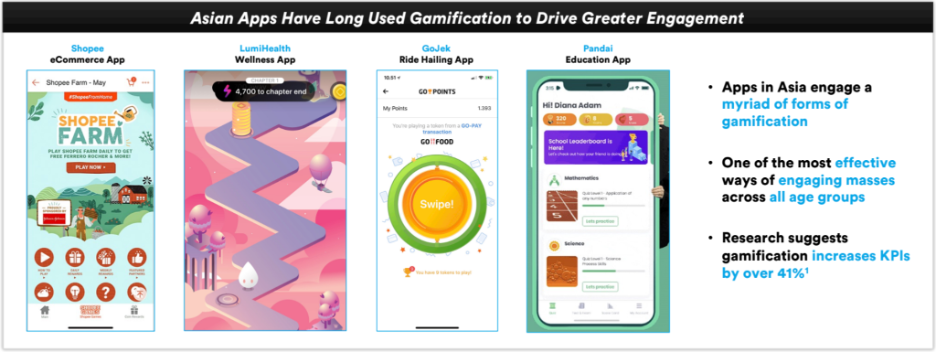

One of our key theses for AGM lies in the belief that teams with a wide-range of experiences and expertise are far more equipped to apply gaming’s best practices to non-gaming use cases today. Asia’s track record of tech startups across an incredibly wide range of tech verticals ranging from fintech to software and even eCommerce speaks to strong foundations in Asia upon which AGM startups have emerged, and we have continued to see non-gaming apps from Asia exhibit relatively higher levels of gamification than non-Asia apps:

Note 1: Salescreen

In the slide above, we took a look at several categorically non-gaming specific apps including Shopee, LumiHealth, GoJek and Pandai which primarily service Asian populations. Compared to western equivalents such as Uber or Amazon, it becomes clear that Asian apps tend to more heavily leverage gamification techniques to better engage with a young and relatively more gaming-native audience. We believe this trend will continue to persist and will result in the emergence of more AGM startups which not only layer on gamification but increasingly build products that subtly incorporate the most effective game design principles and mechanics from the ground up.

BITKRAFT has already invested into two AGM startups within Asia, and now with a more local presence in the region to hunt for these opportunities, Jin and I are hopeful that the portfolio of AGM investments will continue to grow.

Conclusion

In times past, the Silk Road comprised an intricate network of trade routes that once connected the East to the West. It was not merely a pathway for goods but a conduit for ideas, culture, technology, and innovation. The Silk Road transcended borders and brought disparate regions into dialogue with one another, and allowed for the cross-pollination of novel ideas and best practices which advanced all of humanity.

Today, gaming continues to globalise and we continue to see the merging of oceans between the East and the West - from the growing receptiveness of mobile gaming in the West, to the growing desire to produce AAA PC/ Console games here in the East, the complexion of the global gaming market continues to look increasingly like a single shared universe rather than a tale of two cities.

With this ongoing globalisation, there is once again tremendous opportunity for a new Silk Road to emerge, and for BITKRAFT to serve as that conduit for knowledge exchange, technological advancement, and immense economic opportunity. Just as the Silk Road opened up countless opportunities and advanced trade and civilization centuries ago, our mission at BITKRAFT will be to invest into the region, help our portfolio companies access the greatest learnings the world has to offer whichever that region may be, and be the Silk Road of Gaming.